Industry News

Inflation Increases Cost of Workers’ Compensation Claims

Author, Sam Brown, Account Executive, Rancho Mesa Insurance Services, Inc.

As non-profits and leaders of human service organizations navigate important business decisions in the face of inflation, it’s important to consider measures that can reduce inflation’s impact to an organization’s operating budget. Today, we look at inflation’s effect on workers’ compensation insurance and strategies to reduce future costs.

Author, Sam Brown, Account Executive, Rancho Mesa Insurance Services, Inc.

As non-profits and leaders of human service organizations navigate important business decisions in the face of inflation, it’s important to consider measures that can reduce inflation’s impact to an organization’s operating budget. Today, we look at inflation’s effect on workers’ compensation insurance and strategies to reduce future costs.

In August 2022, the U.S. Bureau of Labor Statistics published data reflecting an 8.3% increase to the Consumer Price Index for All Urban Consumers over the previous 12 months. If medical costs are the largest expenditure in workers’ compensation claims, how is the recent inflationary trends affecting worker’s compensation medical and claim costs?

Medical costs per workers’ compensation claim increased almost 18% between 2012 and 2021 according to a study by the National Council on Compensation Insurance (NCCI). Moving forward, the Office of the Actuary at the Centers for Medicare and Medicaid Services projects an index closely related to medical costs in worker’s compensation will increase 2.5% to 3% beyond 2022. Inflation has impacted many segments of the economy, including workers’ compensation insurance.

Strategies to reduce inflation’s impact to workers’ compensation insurance premiums, include:

Offer modified duty to all injured workers.

Offering modified duty to employees with work restrictions is widely known to reduce the likelihood of workers’ compensation litigation and reduces the overall cost and duration of the claim. In addition, if an injured employee rejects the offer, then the individual can no longer receive temporary disability benefits. These positive outcomes may help explain why at least one insurance company offers a 10% rate discount to employers that offer modified duty to all injured workers.

Consider on-call medical technician and telephonic nurse triage services.

Rancho Mesa has published articles about the benefits of on-site medical evaluations and nurse-triage services, but they deserve a fresh look. Both services can advise the injured workers on proper self-care, thereby providing the employee with helpful treatment options while avoiding a costly workers’ compensation claim. The employer will also avoid paying the injured worker’s wages while they travel to and wait inside a medical provider’s office.

The nurse-triage service will continue to manage the injury and help the employee determine if further medical care is necessary. Of course, employers should always report the incident to the workers’ compensation carrier.

Consider an alternative workers’ compensation plan to gain more control over claim and insurance premiums.

It’s true that self-insured worker’s compensation plans are typically reserved for very large organizations, but options exist that replicate some of the most beneficial features. The available options depend on the size of the employer.

Small to medium sized employers can explore self-insured groups (SIG) to potentially split payroll between class codes and receive dividends. SIGs are very motivated to help members avoid workers’ compensation claims, but also closely manage open claims. A member vote is typically required after a review of an applicant’s safety plan, safety record, and operations.

Medium to large organizations may consider loss-sensitive plans. The policy will typically offer reduced annual premium if the employer can control claim frequency and claim costs. There may also be an opportunity to share in the underwriting profit following a plan year. Of course, the insured may also need to share in the claim costs in a poor performing year.

Another alternative, workers’ compensation deductible plans, can also offer a premium savings if the employer is willing to pay a deductible on each claim. Deductibles can range from $10,000 to $100,000 or more, depending on the employer’s risk tolerance.

Looking at alternative workers’ compensation strategies and plans can help employers navigate the current pattern of inflation. The information above can reduce claim frequency, claim cost, and also inform nonprofit and human service leaders about potential insurance premium savings available.

To discuss your organization’s options, contact me at (619) 937-0175 or sbrown@ranchomesa.com.

Important Updates to Minimum Wage Policies for 2023

Author, Megan Lockhart, Media Communications and Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

As businesses ring in the New Year, it is important for owners to note some key changes to state and local wage policies taking effect January 1, 2023.

Author, Megan Lockhart, Media Communications and Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

As businesses ring in the New Year, it is important for owners to note some key changes to state and local wage policies taking effect January 1, 2023.

Established by the Fair Labor Standards Act (FLSA), the federal minimum wage rate stands at $7.25. However, changes to minimum and tipped wages will impact individual states and local areas. In California, the State minimum wage as of January 1, 2023 is $15.50 regardless of tips. Be sure to check the updates to your specific location to ensure your company is best prepared for the New Year.

Local Minimum Wage Rates for California

| Locality | Coverage | Minimum Wage as of January 1, 2023 Increase |

| Alameda City | $15.75 | |

| Belmont | $16.75 | |

| Berkeley | $16.99 | |

| Burlingame | $16.47 | |

| Cupertino | $17.20 | |

| Daly City | $16.07 | |

| East Palo Alto | $16.50 | |

| El Cerrito | $17.35 | |

| Emeryville | $17.68 | |

| Foster City | Employers that have a business license from Foster City | $16.50 |

| Fremont | $16.00 | |

| Half Moon Bay | $16.45 | |

| Hayward | Employers with 25 or fewer employees | $15.50 (state rate) |

| Hayward | Employers with 26 or more employees | $16.34 |

| Long Beach | Hotel employers (100 or more guest rooms) | $16.73 |

| Long Beach | Employers of concessionaires at the Long Beach Airport and Long Beach Convention Center | $16.55 |

| Los Altos | $17.20 | |

| Los Angeles City | General | $16.04 |

| Los Angeles City | Hotel employers with 150 or more guest rooms | $18.17 |

| Los Angeles County (unincorporated areas) | $15.96 | |

| Malibu | $15.96 | |

| Menlo Park | $16.20 | |

| Milpitas | $16.40 | |

| Mountain View | Employers that are subject to the Mountain View Business License Tax or that maintain a facility in Mountain View | $18.15 |

| Novato | Business with 1 – 25 employees | $15.53 |

| Novato | Business with 26 – 99 employees | $16.07 |

| Novato | Business with 100+ employees | $16.32 |

| Oakland | General | $15.97 |

| Oakland | Hotel employers (50 or more rooms) with qualifying health benefits | $17.37 |

| Oakland | Hotel employers (50 or more rooms) without qualifying health benefits | $23.15 |

| Palo Alto | $17.25 | |

| Pasadena | $16.11 | |

| Petaluma | $17.06 | |

| Redwood City | $17.00 | |

| Richmond | Employers that offer qualifying health benefits | $15.50 (state rate) |

| Richmond | Employers that don’t offer qualifying health benefits | $16.17 |

| San Carlos | $16.32 | |

| San Diego | $16.30 | |

| San Francisco | $16.99 | |

| San Jose | $17.00 | |

| San Mateo City | $16.75 | |

| Santa Clara City | $17.20 | |

| Santa Monica | General | $15.96 |

| Santa Monica | Hotel employers | $18.17 |

| Santa Rosa | $17.06 | |

| Sonoma City | Employers with 25 or fewer employees | $16.00 |

| Sonoma City | Employers with 26 or more employees | $17.00 |

| South San Francisco | $16.70 | |

| Sunnyvale | $17.95 | |

| West Hollywood | Employers with 49 or fewer employees | $17.00 |

| West Hollywood | Employers with 50 or more employees | $17.50 |

| West Hollywood | Hotel employers | $18.35 |

Clients can login to the RM365 HRAdvantage™ portal to review the full local minimum and tipped wages for all states and counties under the New Chart: 2023 State and Local Minimum and Tipped Wages.

Construction Death Rate Not Decreasing as Expected

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

With the heightened safety regulations and OSHA guidelines over the past decade, many would think we are working in a much safer environment with fewer fatalities. Despite the rising number of employees and using a standard based off deaths per 100,000 employees, the data is showing that the number of fatalities are the same as they were a decade ago.

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

With the heightened safety regulations and OSHA guidelines over the past decade, many would think we are working in a much safer environment with fewer fatalities. Despite the rising number of employees and using a standard based off deaths per 100,000 employees, the data is showing that the number of fatalities are the same as they were a decade ago.

With a much larger workforce, OSHA is severely understaffed compared to the previous decade. The agency does not have enough inspectors to visit nearly enough jobsites. They have been more reactive in the sense that they are imposing fines on companies after they have had losses. These fines represent a fraction of what it would take to motivate construction companies to revamp their respective safety programs. Employers have factored these fines into the cost of business to a certain extent.

OSHA is now contemplating whether it is worth doubling the jobsite inspections annually and/or increase fines drastically. There is no solid data to link an increase in jobsite inspections to fewer fatalities, so the logical answer would be heavier fines and a push for more negligent death claims to be criminally prosecuted.

Either of these options will lead to more oversite or more fines for the construction industry as a whole. One critical approach you can take is to prepare yourself as a business owner. Be proactive. Consider working with the consultation branch of OSHA to visit your operation and jobsites. This division within OSHA does not issue fines or violations. They do, however, offer recommendations and advice on how to make your operation safer. With the potential of OSHA’s fines increasing, it is time to make sure that your company is on the forefront of safety. A great first step is reaching out to your insurance broker to help you meet requirements and push you to exceed. With a potential recession looming, it is important to make sure you have insulated your company from risk, so you have the best chance at thriving.

If you have any urgent questions on this topic, you can reach me directly at (619) 438-6900 or email me at ccraig@ranchomesa.com.

All Licensed California Tree Care Companies Now Required to Carry Workers’ Comp. Insurance

Author, Rory Anderson, Account Executive, Rancho Mesa Insurance Services, Inc.

Within the last few weeks, all licensed tree care companies received a notice in the mail from the California State License Board (CSLB) stating that effective January 1, 2023, the CSLB is requiring that all companies with a D-49 Tree Service Contractor license must have workers’ compensation insurance, regardless of whether they have employees.

Author, Rory Anderson, Account Executive, Rancho Mesa Insurance Services, Inc.

Within the last few weeks, all licensed tree care companies received a notice in the mail from the California State License Board (CSLB) stating that effective January 1, 2023, the CSLB is requiring that all companies with a D-49 Tree Service Contractor License must have workers’ compensation insurance, regardless of whether they have employees.

Currently, licensed tree care companies without employees are exempt from having workers’ compensation insurance. This new requirement comes after Governor Gavin Newsom signed Senate Bill 216 into law on September 30, 2022 which requires all contractors (not just tree service contractors), with or without employees, to have workers’ compensation insurance by January 1, 2026.

According to an article by Red Bluff Daily News, “The California State License Board research confirms that many of the approximate 50 to 60 percent of licensed contractors who currently claim an exemption to workers’ compensation insurance do use employees.”

This not only puts the non-insured tree workers and the public at risk, but it also poses an issue of unfair advantage to the companies who do not carry workers’ compensation. This creates a disadvantage for tree service contractors who play by the rules, as they are subject to higher business costs.

This new requirement will hold every tree service contractor accountable to the same standards by leveling the playing field, and it will protect the tree workers and our public.

How does this impact you, as a licensed tree service contractor?

If you currently have workers’ compensation insurance in place, confirm with your broker that they have properly provided a certificate of insurance to the CSLB to show proof of insurance. You may also check your license status with the Department of Consumer Affairs to confirm it is up to date.

If you are a tree care company that does not currently have employees, contact me to explore workers’ compensation insurance options for your business, effective January 1, 2023.

If you would like to discuss further, please reach out to me at randerson@ranchomesa.com or call me at (619) 486-6437.

Training Supervisors on Workplace Injury Protocol Can Improve Claim Outcomes

Author, Sam Brown, Account Executive, Rancho Mesa Insurance Services, Inc.

California employers work hard to maintain a safe workplace, but accidents and injuries can occur. While human resources professionals typically have an excellent understanding of the workers’ compensation claim process, proper supervisor training can improve workers’ compensation outcomes for employers and their injured workers.

Author, Sam Brown, Account Executive, Rancho Mesa Insurance Services, Inc.

California employers work hard to maintain a safe workplace, but accidents and injuries can occur. While human resources professionals typically have an excellent understanding of the workers’ compensation claim process, proper supervisor training can improve workers’ compensation outcomes for employers and their injured workers.

Supervisors are often the first to become aware of a workplace injury. Without proper training a supervisor may have the best of intentions, but can create problems by not following company protocols. Sound supervisor training may include:

How to Get the Injured Worker Medical Attention

Supervisors should know the designated medical provider or understand how and when to direct an employee to use telephonic nurse triage services. The supervisor should know what information the provider will need and, if necessary, how the injured worker should be transported to the medical provider’s physical location.

Internal Communication

Supervisors must know how to initiate documenting a workplace injury and how to notify the proper parties of the incident. What incident report should be used? Are witness statements important? Who needs to know of the incident as soon as possible? Whose responsibility is it to report the claim to the insurance company?

Effective Communication

A supervisor setting a tone of empathy immediately following a workplace injury can lead to positive outcomes and reduce the likelihood of litigation. Effective communication can even reduce claim frequency. A study by Shaw, et al., shows how four hours of supervisor training on communication skills and accommodation for workers reporting health concerns produced “a 47% reduction in new claims and an 18% reduction in active lost-time claims.”

Well-designed training can greatly improve workers’ compensation claim outcomes when supervisors follow company protocols, get injured workers medical care, and practice effective communication in the workplace.

Rancho Mesa has developed downloadable forms for the Supervisor’s Report of Employee Accident or Near Miss, and Witness’ Statement to help collect important information about an accident.

For more information on effective workers’ compensation programs, please contact me at sbrown@ranchomesa.com or (619) 937-0175.

Benefits of Offering Modified Work to Injured Workers

Author, Jim Malone, Workers’ Compensation Claims Advocate, Rancho Mesa Insurance Services, Inc.

There are many things the employer is required to do after a work related injury occurs. There are also additional things an employer can and should do after an employee is injured, though not required by any regulatory agency, like offering modified work.

Author, Jim Malone, Workers’ Compensation Claims Advocate, Rancho Mesa Insurance Services, Inc.

There are many things the employer is required to do after a work related injury occurs. There are also additional things an employer can and should do after an employee is injured, though not required by any regulatory agency, like offering modified work.

Obviously, there is the immediate need to address the injury itself. This is usually done by the lead, foreman, or supervisor and would include stopping the bleeding, placing ice on the injured area, etc. The injured worker’s injury then needs to be assessed by a medical professional. There are options for having the injury medically assessed. For minor injuries, it may be by calling a triage service or having a medical triage specialist (nurse or paramedic) go to the injured worker to determine if this minor injury can be taken care of with self-care or if the injured worker needs to be seen at an occupational medicine clinic. With referring your injured worker to a clinic, you should determine if the injured worker can drive themselves or if they need a company representative to drive them.

After the injury is properly addressed, focus on the reporting of the claim. Gather the forms and reports that need to be completed or obtained to provide to the insurance adjuster. Your next decision comes after the treating physician completes their initial evaluation. The physician should provide doctor notes, the mechanism of injury, how the injury occurred, and any other additional information. The physician may also provide wound care, sutures, x-rays, ace wraps, medications, ointments and make referrals for physical therapy, acupuncture and/or chiropractic treatment, etc.

The treating physician then provides their recommendations on the injured worker’s ability to return to work. For more severe injuries, the treating physician may want the injured worker to remain off work completely and could recommend temporary total disability. After some time off work and with some provided treatment, the doctor usually recommends that the injured worker return to work, but with some restrictions, such as not lifting over a certain amount of weight, not exceeding so many hours of weight bearing, etc. The restrictions provided are usually consistent with the body part(s) that were injured.

So, the treating physician is releasing the injured worker to return to work but not to full, physical capacity. This is called a release to modified work, restricted duties, or light duties. From the insurance claims perspective, this is referred to as temporary partial disability. The modified work restrictions are usually slowly decreased while the injured worker continues the treatments and recovers from the work injury. This gradual recovery continues until the injured worker is able to resume all their physical work activities. This is called being released to full work activities, unrestricted duties, or to their usual and customary duties.

When the injured worker is released to modified work (i.e., restricted, light) duties, the employer decides if they can provide the injured employee duties that allows them to work while avoiding certain physical activities consistent with the doctor’s return to work recommendations.

Benefits to the Employee

Providing modified, restricted, light duty work serves many purposes. First and foremost, providing modified work can reassure an injured worker that their employer cares for them personally, professionally, and psychologically. A work injury can be a very traumatic event, and returning to work as soon as possible after a work injury can help the injured worker feel confident their employer will be there for them and their family as they recover from the accident. This is one of the ways the employer can show their support of, and gratitude for, their employees and all the hard work they provide.

Many studies have shown that providing modified work results in injured workers recovering quicker and more completely. It allows the injured worker to maintain their earnings and usual working schedule, while maintaining their relationships with the foreman, supervisors, and co-workers. Modified work also allows the injured employee to remain physically and mentally active while also allowing them to focus on their treatment and recovery.

Effect on the Business

For a business, a work injury can be very disruptive. The disruption of a work injury usually causes employers to move employees around to compensate for a lost employee. Employees working together as a team would see a change in work partners. Crews would be short a person who would be responsible for a certain part of an assignment resulting in changes in each crew member’s responsibilities. A work injury may affect how quickly the team can complete a job or project, how quickly the crew completes their daily tasks, and even how the employer is able to bid on future jobs or projects.

Work injuries are stressful for an employer and the remaining employees. Besides the lost productivity from an injured worker, there may also be an emotional strain to other employees, or concerns about their own safety, about how they would be able to handle such an injury or how they would be treated if they were injured.

Assigning an injured worker to modified work allows the employer to address other items of their business that may not get addressed when all employees are working at full capacity or when there are not enough employees to address these other areas. Assigning an injured worker to modified duties can allow an employer get caught up on cleaning certain areas, re-organizing a storeroom, updating inventory, etc.

Benefits to the Business

Providing modified work allows an employer to have a direct impact on the overall cost of a work-related injury claim. By providing modified work, the employer pays the injured worker’s wages instead of the claims adjuster paying temporary disability benefits. If the employer does not offer modified work for an injured worker, instead of being temporarily partially disabled, the injured worker is then considered temporarily totally disabled. The claims adjuster would then be required to pay the injured worker temporary disability benefits at 2/3 of the injured worker’s average weekly wage. This is calculated from the 52 weeks of previous earning information you provide the adjuster when the claim was being created. This is also a tax-free benefit.

However, getting these temporary disability benefits can also be a disincentive for injured workers to return to their normal work duties sooner than they are required. There is an increasing trend of injured workers refusing to return to modified work offered by their employers. Whether they want to stay home and collect temporary disability benefits, complete a side job they were working on while concurrently working for the employer, or if they believe they will recover quicker by simply staying home, injured workers can make it difficult to provide modified work. They can be disruptive, argumentative and provide poor quality of work while performing modified work. They can be insubordinate while performing modified work and can arrive late, leave early, take too much time for doctor or treatment appointments, etc. They can frustrate the employer so much that the employer may want to reconsider offering modified work to this injured worker. If the employee declines the employer’s modified work offer, the injured worker would no longer receive any wages from the employer and they would not be entitled to any temporary disability benefits/payments from the adjuster.

Injured workers retain legal counsel for work-related injuries for a wide variety of reasons. Disagreements over returning to modified work is one of the most common of these reasons. When an attorney becomes involved in a workers’ compensation claim, there are usually disagreements over a number of issues, but the modified work dispute from the attorney is usually that the employer did not properly advise or instruct the injured worker about their responsibilities related to modified work offers.

The lost time from work issue, after modified work is declined by the injured worker, usually becomes a monetary issue that is documented at the time, then later becomes one of the issues to negotiate or resolve when the claim is being settled. Usually a dispute like this is negotiated somewhere between the full value of the time lost from work and zero. This adds to the overall cost of a workers’ compensation claim. The development of this issue, however, can be completely avoided if the employer were to document the offer of modified work in writing. The employer can draft their own offer of modified work letter. The claims adjuster, their return to work specialists, or your claims advocate can also provide assistance with drafting of this letter.

When an injured worker declines modified work offers, they sometimes get state disability benefits from the State of California Employment Develop Department (EDD), who in turn file a lien (or bill) for the lost time benefits paid to the injured worker on the workers’ compensation claim. If the attorney and the claims adjuster are unable to resolve this issue, the documentation obtained (The Modified Work Offer letter) when the modified work was offered will usually be sufficient evidence for not reimbursing EDD for any of their lien, and/or for the workers’ compensation judge to agree with the employer and claims adjuster on this issue.

Offering modified work is a very good thing to do for injured workers, for their recovery, and for the employer. It is also a very effective and proven strategy for handling workers’ compensation claims. Offering modified work can speed up the injured worker’s recovery. This allows the workers’ compensation claim to move quicker through the claim process to resolution or settlement. This usually results in the injured worker’s return to their normal work activities, their continued employment with the employer, and in reducing the cost of the workers’ compensation claim.

Roofing Contractors Prepare for the Dual Wage Threshold Increase

Author, Kevin Howard, Account Executive, Rancho Mesa Insurance Services, Inc.

There is a lot at stake for roofing contractors in California. Many of us recall playing the game “would you rather” as kids. Would you rather jump into a freezing cold pool in December or eat the world’s hottest chili pepper with no milk available?

Author, Kevin Howard, Account Executive, Rancho Mesa Insurance Services, Inc.

There is a lot at stake for roofing contractors in California. Many of us recall playing the game “would you rather” as kids. Would you rather jump into a freezing cold pool in December or eat the world’s hottest chili pepper with no milk available?

For roofers across the state, the question for them is, “would you rather give strategic pay raises to key employees or pay higher than necessary worker’s compensation premiums?” The ideal solution would be to give appropriate pay raises to help retain quality employees and to pay less for worker’s compensation.

To get into the math, the Workers’ Compensation Rating Bureau (WCIRB) has increased the dual wage threshold for the roofing class codes 5552 and 5553 by $2. The prior wage threshold was $27 per hour. The change that went into effect September 1, 2022 adjusted the new wage threshold to $29 for these same codes.

So, any roofers renewing on or after September 1, 2022 will need to explore what makes the most sense regarding the hourly wages of their employees.

This increase for roofing contractors is critical to understand because of the massive rate difference between class code 5553 ($29 or more per hour) and (under $29 per hour).

To drill down further, we analyzed the base rates for class codes 5552 and 5553 from 10 different worker’s compensation carriers. The average delta in base rates was 65%. That is a huge swing in cost for any roofing contractor who is not familiar with the cost benefit analysis that must take place.

As an example, we will use $1 million in payroll for 3 different scenarios to help paint a picture of this wage threshold change.

SCENARIO #1:

ABC Roofing has $1 million in payroll and all employees make $27 per hour. Using a hypothetical net rate of $40 for class code 5552, the insurance premium for scenario #1 would be $400,000.

SCENARIO #2:

XYZ Roofing has $1 million in payroll and all employee make $29 per hour. Using a hypothetical net rate of $14 (which is 65% less than $40), the projected workers’ compensation annual estimated premium would be $140,000.

SCENARIO #3:

ABC’s insurance agent made them aware of the new wage threshold increase well in advance of their renewal. They gave appropriate wage increases to 75% of employees and now have $250,000 of payroll in class code 5552 and $750,000 in class code 5553. Using the same hypothetical net rates from scenarios #1 and #2, the worker’s compensation annual estimated premium would be $205,000.

In conclusion, the massive delta in base and net rates for the roofing class codes 5552 and 5553 requires a proactive approach with your broker in advance of your upcoming workers’ compensation renewal. Laying out options that can include strategic pay increases can and will ultimately bring significant premium savings to your roofing company. With inflationary costs across all trades trending upward, build a plan now to help offset these rising costs.

To learn more about this topic or have a conversation with us, please email me at khoward@ranchomesa.com or call (619) 438-6874.

Rise in Pure Premium Rates Impacts Tree Care Industry

Author, Rory Anderson, Account Executive, Rancho Mesa Insurance Services, Inc.

Pure premium rates are determined by the Workers’ Compensation Insurance Rating Bureau (WCIRB). The rates reflect the amount of losses that an insurance carrier can expect to pay out in claims for that particular class of business. Every year, the WCIRB submits pure premium rates to the California Department of Insurance for approval. These pure premium rates are comprised of loss and payroll data submitted to the WCIRB by all the insurance companies in California.

Author, Rory Anderson, Account Executive, Rancho Mesa Insurance Services, Inc.

Pure premium rates are determined by the Workers’ Compensation Insurance Rating Bureau (WCIRB). The rates reflect the amount of losses that an insurance carrier can expect to pay out in claims for a particular class of business. Every year, the WCIRB submits pure premium rates to the California Department of Insurance for approval. These pure premium rates are comprised of loss and payroll data submitted to the WCIRB by all the insurance companies in California.

Each workers’ compensation insurance company has its own base rate for the 0106 Tree Pruning class code, for example. In order to establish the base rate, the insurance carrier takes the approved pure premium rate from the WCIRB and applies their factor that includes general overhead expenses, sales and marketing expenses, taxes and fees, and profit. So, if the pure premium rates are increasing, the insurance companies’ base rates are also increasing.

The 2022 pure premium rate in the tree care industry (class code 0106) has increased to $11.36 per $100 of payroll, which is roughly a 9% increase from last years $10.39. This means that the overall workers’ compensation claim activity in the tree care industry is up about 9%, and the WCIRB is recommending that the workers’ compensation insurance carriers increase their base rates to price for that increase in claim activity.

What can you do to prepare for this change and limit the impact to your tree care business?

Lower your claim frequency and severity with a consistent, robust safety and training program, focusing in on root causes of the claims.

Control your experience MOD with quarterly claim reviews and an aggressive return to work program.

Maintain strong carrier partnerships and continuity with carriers that have excellent in-house claims handling.

Benchmark your company with the rest of the tree care industry to see how you compare to your peers. As part of our proprietary TreeOne™ program, we have created a Key Performance Indicator (KPI) dashboard for the tree care industry that puts this information at your fingertips. To see how you compare with your peers, request the KPI Dashboard for your company.

For more information on rising pure premium rates, contact me at (619) 486-6437 or email me at randerson@ranchomesa.com.

The Link Between Your EMR and Primary Threshold

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

One of the biggest concerns for contractors is their Experience Modification Rating (EMR). If your EMR exceeds 1.00 or 1.25, contractors can be removed from bid lists and premiums can escalate quickly. Most decision makers have little idea what factors contribute to the EMR and just how claims can impact them.

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

One of the biggest concerns for contractors is their Experience Modification Rating (EMR). If your EMR exceeds 1.00 or 1.25, contractors can be removed from bid lists and premiums can escalate quickly. Most decision makers have little idea what factors contribute to the EMR and just how claims can impact them.

All construction companies are assigned class codes that best define their operations and those class codes have expected loss rates associated with them. The more losses that occur per $100 of payroll for that class code, the larger the expected loss rate will be. So, an electrician with a much lower expected loss rate than a roofing contractor will have each claim impact their EMR more. These are variables that can have a significant impact on your company’s EMR. The variable that fluctuates amongst each company is the amount of payroll they develop in each class code. The more payroll generated, the lower your best possible EMR can be.

Consequently, as a company’s best possible EMR decreases, the Primary Threshold increases. The Primary Threshold is a cap or threshold unique to each company. The higher the primary threshold, the less that any one claim can impact your EMR. For example, a painting contractor using the 5474 class code and averaging $200,000 a year in payroll will have a best possible EMR of 83 and primary threshold of only $8,500. Each claim has the potential of contributing 40 points to their EMR. While another painter that averages $10,000,000 in payroll will have a best possible EMR of 41 and primary threshold of $49,000. Thus, the maximum any one claim can impact the company with higher payroll is just 5 points.

This certainly is a drastic difference but it makes sense as the larger company has more employees which leads to more exposure and more expected losses. The component that most companies do not know well enough is that for each company in the examples above, the WCIRB penalizes the exact same for any claim that exceeds your primary threshold. So, for the smaller company, an $8,500 claim is worth 40 points to their EMR, a $1,000,000 claim is worth the exact same amount. And, the same for the larger company with a $49,000 claim worth 5 points but any claim dollars in excess of that will not impact the EMR.

Taking this information into account, we urge our clients to focus on mitigating claims before they happen as well as doing their best to reduce contributing factors such as temporary disability. Having your carrier pay for your employees missed time leads to your EMR increasing and your premiums inevitably being higher than you would like.

Understanding and implementing a return-to-work program is extremely beneficial to your company and leads to you saving money over time. Working with your broker to better understand how to properly handle claims and making sure you are doing everything possible to keep your EMR as low as possible is vital to your company’s profitability and is very much in your control.

Everyone wants a better EMR and lower premiums but the elite contractors are active in not only preventing claims from happening but understanding how important it is to keep their employees at the workplace, or at the very least, off the couch at home.

If you would like to learn more about your firm’s primary threshold or how it is impacting your company, please do not hesitate to reach out to me directly at ccraig@ranchomesa.com or call me at (619) 438-6900.

California Insurance Commissioner Leaves Workers’ Comp Rates Flat

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

California Insurance Commissioner Ricardo Lara released a statement that he is rejecting the Workers’ Compensation Insurance Rating Bureau’s (WCIRB) recommended 7.6% increase in the workers’ compensation pure premium rates as well as the add-on to cover COVID-19 claim costs. The Commissioner also rejected a more modest 2.8% increase recommended by the Department of Insurance’s actuaries and the 1.4% decrease recommended by an independent actuary for the public members of the Bureau’s governing committee.

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

California Insurance Commissioner Ricardo Lara released a statement that he is rejecting the Workers’ Compensation Insurance Rating Bureau’s (WCIRB) recommended 7.6% increase in the workers’ compensation pure premium rates as well as the add-on to cover COVID-19 claim costs. The Commissioner also rejected a more modest 2.8% increase recommended by the Department of Insurance’s actuaries and the 1.4% decrease recommended by an independent actuary for the public members of the Bureau’s governing committee.

Commissioner Lara’s decision was based on California’s still recovering economy. With businesses trying to recover to pre-pandemic levels and the uncertainty still of COVID-19 disruptions, the Commissioner decided to keep the benchmark rate of $1.45 per $100 of payroll. Keep in mind that the pure premium rate is only advisory as the Commissioner does not have rate setting authority over workers’ compensation rates. In fact, the rate level of $1.45 is actually 18% lower than the industry filed average pure premium rate of $1.77 as of January 1, 2022.

“We’re working hard to get California back to business as usual as people return to work,” said Lara. “This year’s rate is on par with normal, pre-pandemic levels while still reflecting the long-term benefits of workers’ compensation reform passed by the State Legislature and signed by the Governor to reduce costs.”

With signs of a hardening market such as increased carrier combined ratios, increased cost on indemnity claims, medical inflation, and future costs of COVID-19 claims, it will be interesting to see how carriers will respond to this decision. Now, more than ever, it is critical to work with your broker and carrier to improve your risk management program so that your business is positioned well for the future.

If you are interested in how this process works and how it can improve your bottom line, please reach out to me at (619) 937-0174 or jhoolihan@ranchomesa.com. In the meantime, Rancho Mesa will keep close tabs on what the future holds and communicate updates regularly.

Proposal to Include COVID-19 Claims in EMR Calculation is Denied

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

It appears the COVID-19 pandemic has finally entered an endemic stage and most companies have fully re-opened and/or are offering their employees some type of a hybrid work schedule. With this being the case, the California Workers’ Compensation Insurance Rating Bureau (WCIRB) proposed to amend the rule that excludes COVID-19 claims from the calculation of experience modifications for only claims with incident dates from December 1, 2019 through August 31, 2022.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

It appears the COVID-19 pandemic has finally entered an endemic stage and most companies have fully re-opened and/or are offering their employees some type of a hybrid work schedule. With this being the case, the California Workers’ Compensation Insurance Rating Bureau (WCIRB) proposed to amend the rule that excludes COVID-19 claims from the calculation of experience modifications for only claims with incident dates from December 1, 2019 through August 31, 2022. In addition, the WCIRB proposed that effective September 1, 2022, any new COVID-19 claims occurring after this date would be factored into the calculation of an employer’s experience modification rate.

The WCIRB’s rationale for this recommendation was that current circumstances have greatly changed since the rule to exclude COVID-19 claims from the experience rating were initially adopted in 2020. COVID-19 is no longer a temporary short-term phenomenon and the risk of infection will be present in the general population for the foreseeable future.

With workplace safety standards in place, personal protective equipment and vaccinations available, employers who are diligent in protecting their employees would in turn have a lower experience modification than less safety-conscious employers in the same industry.

Fortunately, in late June 2022, this change was not approved by Commissioner Lara, but employers should still actively try to prevent the spread of COVID-19 within the workplace by having a written COVID-19 prevention program in place and follow the requirements set by the state and local health department.

While employers don’t have to worry that COVID-19 cases will affect their experience modification rate, they should still be concerned about the effects on their employees and bottom line. Having employees miss work because of COVID-19 puts extra strain on other employees and can effect productivity, and thus profitability.

Rancho Mesa has updated its COVID-19 Prevention Program Template designed for California businesses. Request your COVID-19 Prevention Plan template online or contact me at sclayton@ranchomesa.com or (619)937-0167.

Dashboard Spotlight: Your Path to an Experience MOD Below 1.00

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

Rancho Mesa’s Safety KPI Dashboard allows businesses the ability to clearly visualize their path to an Experience MOD (XMOD) below 1.00 through goal setting.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

Rancho Mesa’s Safety KPI Dashboard allows businesses the ability to clearly visualize their path to an Experience MOD (XMOD) below 1.00 through goal setting.

In order to set your business goal, you will need to use three available metrics from your custom dashboard.

Lowest Possible XMOD – This is the best case scenario if you had zero claims for the three-year XMOD period.

Claim Cost Per 1 XMOD Point – This is the amount of incurred claim cost that impacts your XMOD by 1 point.

Unit Stat Date – This is the moment when your information is sent to the rating bureau for next year’s XMOD to be calculated.

Using these three metrics together, you can effectively set your goal and manage your XMOD accordingly.

The XMOD is calculated using a running three-year window of the most recently completed workers’ compensation policies. Each policy period will contribute a set amount of weight on the XMOD calculation based on payroll and claims.

Take your lowest possible XMOD from the KPI dashboard and subtract that number from .99.

You will be left with the amount of XMOD points your company can absorb while still keeping your XMOD below 1.00.

Divide that number by three and you can evenly distribute the amount of XMOD points you can have each year to keep your XMOD below 1.00.

Take the annual XMOD points and multiple by your Claim Cost Per 1 XMOD Point.** This will give you the maximum claim cost available per policy period.

Example:

Lowest Possible XMOD: 47

Claim Cost Per 1 XMOD Point: $3,100

Unit Stat: September 30th

(.99) – (.47) = .52 (Number of XMOD points available to absorb and keep XMOD below 1.00)

(.52) / (3) = 17.3 (Max XMOD points per year)

(17.3) * (3,100) = $53,630 (Max claim cost available per policy period) **

**Must consider your primary threshold, which is also a number available on the KPI Dashboard.

Knowing these numbers, along with when your unit stat date comes up, allows you to strategically plan.

If all of this seems complicated or you just want to see what your company’s dashboard would look like, request a personalized KPI Dashboard and we can discuss how you can develop a path to an XMOD below 1.00.

WCIRB Approves 2022 Construction Dual Wage Threshold Increase

The Workers' Compensation Insurance Rating Bureau (WCIRB) has approved the recommended increase in hourly wage thresholds for all 16 construction dual wage classifications. The increases range from $2 to $5 depending on the classification and will go into effect for policyholders renewing September 1, 2022 and thereafter. The chart below outlines the increases for each classification.

The Workers' Compensation Insurance Rating Bureau (WCIRB) has approved the recommended increase in hourly wage thresholds for all 16 construction dual wage classifications.

The increases range from $2 to $5 depending on the classification and will go into effect for policyholders renewing September 1, 2022 and thereafter. The chart below outlines the increases for each classification.

| Dual Wage Classifications | Existing Threshold | Approved Increase |

Approved Threshold |

| 5027/5028 Masonry | $28 | $4 | $32 |

| 5190/5140 Electrical Wiring | $32 | $2 | $34 |

| 5183/5187 Plumbing | $28 | $3 | $31 |

| 5185/5186 Automatic Sprinkler | $29 | $3 | $32 |

| 5201/5205 Concrete Work | $28 | $4 | $32 |

| 5403/5432 Carpentry | $35 | $4 | $39 |

| 5446/5447 Wallboard Installation | $36 | $2 | $38 |

| 5467/5470 Glaziers | $33 | $3 | $36 |

| 5474/5482 Painting Waterproofing | $28 | $3 | $31 |

| 5484/5485 Plastering or Stucco | $32 | $4 | $36 |

| 5538/5542 Sheet Metal Work | $27 | $2 | $29 |

| 5552/5553 Roofing | $27 | $2 | $29 |

| 5632/5633 Steel Framing | $35 | $4 | $39 |

| 6218/6220 Grading/Land Leveling | $34 | $5 | $39 |

| 6307/6308 Sewer Construction | $34 | $5 | $39 |

| 6315/6316 Water/Gas Mains | $34 | $5 | $39 |

With the continuing labor shortage in construction, employers have been doing everything possible to retain employees by offering richer benefits plans, pay increases and merit bonuses, when applicable. These approved wage classification increases could potentially push employers to extend additional pay raises to employees in an effort to minimize workers’ compensation premiums.

Rancho Mesa predicts that this information will become a major factor in payroll decisions based on overhead cost management and recommend this as a topic for discussion early, so that our clients and prospects can prepare.

Understanding the Impact of MEP Contractors’ Dual Wage & Total Temporary Disability

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

What is a dual wage threshold? According to the Workers’ Compensation Insurance Rating Bureau (WCIRB), in California there are sixteen (16) construction operations that are divided into two separate classifications based on the hourly wage of the employee. There are different advisory pure premium rates for the low wage employee and the high wage employee.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

What is a dual wage threshold? According to the Workers’ Compensation Insurance Rating Bureau (WCIRB), in California there are sixteen (16) construction operations that are divided into two separate classifications based on the hourly wage of the employee. There are different advisory pure premium rates for the low wage employee and the high wage employee. For mechanical, electrical and plumbing (MEP) contractors, the class codes used are all included in the recently approved increase which will go into effect September 1, 2022. The table below outlines the changes for the MEP class codes by year.

| Classifications | 9/1/2021 - Current | 9/1/2022 - Proposed |

| 5140/5190 | $32 | $34 |

| 5183/5187 | $28 | $31 |

| 5538/5542 | $27 | $29 |

© 2021 Workers' Compensation Insurance Rating Bureau of California. All Rights Reserved.

Why does this matter to MEP contractors? The higher wage employee’s workers’ compensation rate is significantly less (on average 46% less) than the lower wage employee. Therefore, if a company has any employees that are currently just barley in the high wage classification, this would drop those employees into the low wage classification and the employer would pay the higher workers’ compensation rate on those individuals. Depending on how many employees an employer has in this situation, it may be advantageous for the employer to calculate if it makes more sense to give those impacted employees a raise to push them back up into the high wage classification or keep them in the new low wage classification. It should be noted and understood that this change will not impact the employer until their next renewal after September 1, 2022. So while most employers will have time to evaluate the impact, it is crucial to begin the evaluation sooner rather than later.

As with any form of wage inflation, an increase in wages, to keep an employee in the higher wage category will increase the claim costs of a total temporary disability claim if they are injured on the job. While increases in wages are necessary, they will also impact the total cost of the claim, which then can increase the company’s experience modification rating (XMOD).

To mitigate this increase and reduce the likelihood of a lost time claim, employers can take several actions:

Review and update their existing safety programs.

Revisit their hiring practices.

Develop a sustainable return-to-work program.

What should employers do next?

Work with your trusted insurance advisor and run a needs/benefit analysis on increasing employee wages.

Understand your numbers.

What is your primary threshold and why does it matter?

What is my claim cost per point of XMOD?

How does my frequency of claims compare to the MEP industry?

How does my lost time claim average compare to other MEP contractors?

If you would like assistance understanding how these and other data points impact your company, request a proprietary Key Performance Indicator (KPI) dashboard that puts this information at your fingertips.

You still have time to be proactive, do not let these critical changes catch you by surprise!

CA Insurance Bureau Recommends 7.6% Rate Increase

Author, Jack Marrs, Associate Account Executive, Human Services Group, Rancho Mesa Insurance Services, Inc.

The Workers’ Compensation Insurance Rating Bureau of California (WCIRB) voted to submit a September 1, 2022 Pure Premium Rate Filing to California’s Insurance Commissioner Lara.

Author, Jack Marrs, Associate Account Executive, Human Services Group, Rancho Mesa Insurance Services, Inc.

The Workers’ Compensation Insurance Rating Bureau of California (WCIRB) voted to submit a September 1, 2022 Pure Premium Rate Filing to California’s Insurance Commissioner Lara.

The filing will suggest a 7.6% average rate increase above last year’s approved September 1, 2021 pure premium rates.

There are multiple reasons for the WCIRB’s Governing Committee to suggest the rate increase. Most notably,

There is an 11% projected increase to indemnity claim cost by the end of 2024.

The industry predicts a 6.5% increase in medical costs per claim from 12/31/21 to 12/31/24.

We expect increases in frequency of injuries and claims.

Wage inflation will increase claim cost and the cost to adjust claims.

Expected future costs of COVID-19 claims are likely to increase, which were previously excluded when underwriting considers claims history.

Before the increase goes into effect, the WCIRB will submit a proposal to the Department of Insurance. Insurance Commissioner Lara will decide to either approve the rate increase, or reject it and suggest a different outcome.

Although the commissioner cannot mandate any sort of rate increase or decrease, it is common for workers’ compensation carriers to cooperate with his recommendation and follow his lead.

This news is another sign that the California workers’ compensation insurance market may be hardening. With that in mind, it is crucial that employers are implementing trainings and safety programs to ensure workplace safety.

In addition, a strong broker partner must truly understand the clients’ industry, operations, and service needs.

Please contact Rancho Mesa to understand how to better prepare for an increase in claims costs and the hardening workers’ compensation marketplace.

Work-Related Automobile Accidents and Their Correlation With Workers’ Compensation Claims

Author, Kevin Howard, Account Executive, Rancho Mesa Insurance Services, Inc.

In California, motor vehicle accidents are among the leading cause of severe injuries on a daily basis. From a risk management perspective, a company’s fleet safety program has a primary goal of keeping employees safe while driving which lowers the amount of annual auto premiums paid.

Author, Kevin Howard, Account Executive, Rancho Mesa Insurance Services, Inc.

In California, motor vehicle accidents are among the leading cause of severe injuries on a daily basis. From a risk management perspective, a company’s fleet safety program has a primary goal of keeping employees safe while driving which lowers the amount of annual auto premiums paid.

What is not typically discussed when talking about fleet safety is the impact a work-related auto incident has on a workers’ compensation policy and experience modification. This article will discuss some of those impacts.

EXPERIENCE MODIFICATION IMPACT

When broken down, workers’ compensation premiums are driven by many factors. A main factor for pricing is the experience modification. Experience modifications are a measure of safety for a company when compared to others in the same field. Workers’ compensation claims adversely affect experience modifications.

Typically, business owners invest time, energy and resources into their safety program in the form of personal protective equipment (PPE), stretching before labor, tailgate meetings and job hazard analysis. But, the “big claim” businesses are doing so much to avoid could come from an auto incident. A heavy dose of fleet safety training should be mixed into the safety topic agenda, tailgate meetings and discussions regarding minimal driving record requirements for employees to drive on behalf of a company.

Businesses in California are required to offer no-fault workers’ compensation insurance which means it doesn’t matter who is at fault, the injury will be covered by a worker’s compensation carrier.

When a work-related auto accident occurs and there is an injury involved with an employee, the experience modification will be affected adversely based on the incurred cost of the claim as well as the loss ratios.

SUBROGATION

If another party is at fault regarding a workers’ compensation claim, the insurance carrier who is tending to the claim can subrogate and try to recoup the paid amount from the responsible party.

The issue workers’ compensation carriers deal with regarding subrogating auto claims is that the California minimum required auto liability limit is only $5,000. This amount would not cover most injuries suffered by an employee in an auto accident. Also, there is a high percentage of drivers who are uninsured which makes subrogation impossible in a claim scenario.

Overall, subrogation is pretty difficult in this specific area of workers’ compensation. The best defense is to avoid auto incidents as much as possible.

MULTIPLE EMPLOYEE IN ONE VEHICLE

Especially with gas prices soaring, carpooling to jobsites can be a popular method of getting employees from one location to the next. Regardless of fault, this could create multiple workers’ compensation injuries at once. Multiple workers’ compensation claims will adversely affect experience modifications, loss ratios and DART rates.

These factors should be considered when creating a car pool scenario for employees travel from jobsite to jobsite.

Important factors to consider if you do utilize carpooling to jobsites could be:

Does the driver meet out company standards with his or her driving record?

Is the vehicle’s maintenance up to date? (e.g., tires, windshield wipers, etc.)

Are there multiple high wage earners traveling in the same vehicle?

TEMPORARY DISIBILITY COST ON THE RISE

With a major labor shortage occurring in California, wages have risen in order to attract and retain labor and highly qualified employees. A severe motor vehicle accident which creates a worker’s compensation claim could adversely affect an employer’s experience modification because two-thirds of the amount of the injured workers’ pay is a larger dollar amount on average than it has been in the past.

This could create a larger claim because of the amount of temporary disability being paid while an employee is hospitalized or unable to come back to work with or without restrictions.

FLEET SAFTEY CONTROLS

When budgeting for an overall safety program, business owners should factor in the multitude of impacts that an auto claim can have on a business. Controls like GPS/telematics, drug testing kits, MVR pull programs, and vehicle maintenance programs are examples of investing in fleet safety.

Fleet safety programs can save lives, save money and can create a stronger culture of safety throughout a business.

Rancho Mesa’s Risk Management Center has a searchable safety library with fleet safety materials that can be used to train employees. Register online for Rancho Mesa’s Fleet Safety webinar on May 26, 2022 from 9:00 am PDT – 10:00 am PDT. Or, contact me at khoward@ranchomesa.com or (619) 438-6874 if you have questions about your auto policy.

Is Now the Time for a Performance-Based Insurance Program?

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

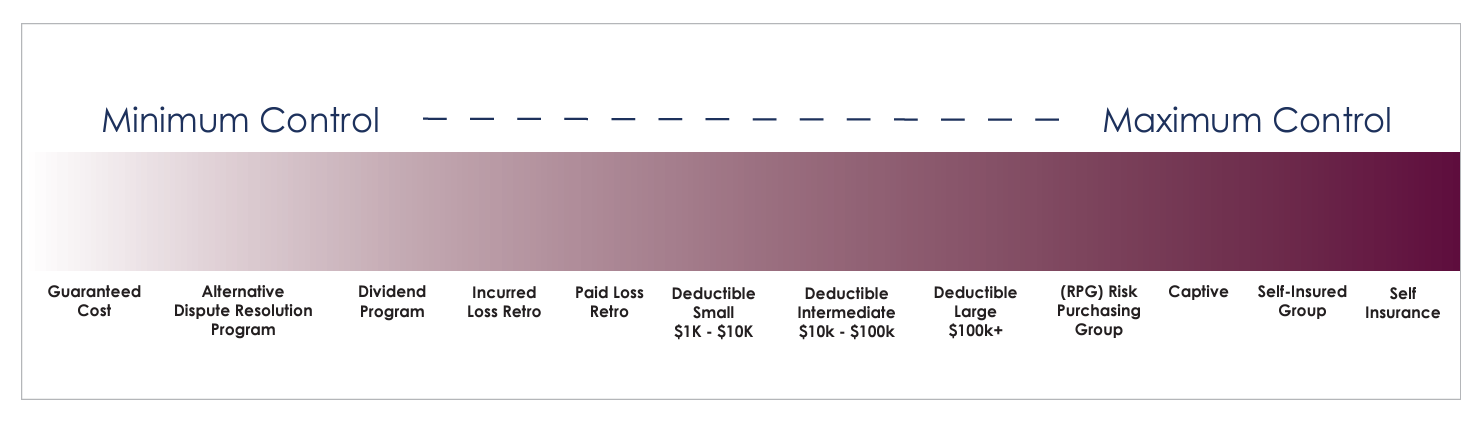

In the three preceding articles in this series, we took a deep dive into some areas where a business’s productivity and profitability could be impacted by various factors emerging in the insurance marketplace. In the course of those articles, we also examined some tools, strategies and ideas that a company might implement to help manage and mitigate those impacts. Today, we will look at a way to exert the most control over your insurance program and premium outcome through performance-based insurance programs.

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

In the three preceding articles in this series, we took a deep dive into some areas where a business’s productivity and profitability could be impacted by various factors emerging in the insurance marketplace. In the course of those articles, we also examined some tools, strategies and ideas that a company might implement to help manage and mitigate those impacts. Today, we will look at a way to exert the most control over your insurance program and premium outcome through performance-based insurance programs.

I’ve written about these programs before in "Increasing Your Productivity and Profitability Through Your Insurance Program," "What is the True Cost of a Lost Time Workers’ Compensation Claim?" and "How is Payroll Inflation Impacting Your Workers' Compensation Premium." So, in lieu of diving into all of them, let’s review a few of them briefly and then spend a little more time with “are they right for you now?”

Beyond guaranteed cost programs, where policyholders pay a set premium and then claims are covered up to the policy limit, there are a wide range of performance-based insurance programs that can apply to a single line of coverage, like workers’ compensation, or multiple lines of coverage that can also include most notably general liability and automobile. Rancho Mesa has created a Workers’ Compensation Continuum document that lists many of these programs. As you move from right to left on the continuum, business owners increase control as well as risk. So, a wise strategy would be to evaluate as many programs as seem to fit your tolerance and readiness for that additional exposure.

Are you confused, yet? You are not alone, which is why it is even more important to start the process with a trusted advisor (your insurance broker) who is both familiar with and skilled in putting these programs in place. A properly skilled and educated advisor will be able to walk you through each option and present it in a way that makes your understanding of it easy to comprehend. If you do not fully understand both the benefits and the risk, we recommend pausing before moving forward, and take ample time for the best decision possible.

As someone who owns and operates a business, I like the idea of the “bet on yourself” model which always makes me feel more in control of the outcome. I cannot emphasize enough how confident you need to be in the ability to control your claims in order for these programs to work for you. That is why in the previous three articles, we talked so much about what you can do to improve your safety programs and more importantly your safety culture. Once you have the right team in place, have reached the point where you have control of your claims, and want more control over your premiums and pricing, then it may to time to move into the performance-based insurance program world.

If my forecast of a hardening workers’ compensation market as early as late 2022 or early 2023 is accurate, then getting started now in putting the right team together should be a priority. Follow these three steps to prepare:

Review your existing safety programs.

a. Look for ways to improve them based on loss trends and industry benchmarks.

Evaluate your claims history over the last five years.

a. Look for the root causes that are driving the losses.

Identify someone internally to be your safety director.

a. Consistently demonstrate upper management’s support of their efforts to the company and make sure you provide them with tools necessary to accomplish their goals.

Finally, in closing, choose a trusted insurance advisor who understands your industry, your operations and is very familiar with performance-based programs. There are good trusted advisors out there, so if you are currently with one, then give them the time they need to help you get better.

If you want to learn more about performance-based programs and would like to talk with us about the opportunity to be your trusted advisor, contact us and our team that specializes in your industry will reach out to you. If you would like to speak with me directly, email me at dgarcia@ranchomesa.com.

I hope you found this series helpful in making your 2022 the most productive, profitable and safe year ever.

How Higher Average Pay Can Lead to Work Comp Savings

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

Wage thresholds have increased consistently in the past decade. This has pushed owners to give sizable raises every few years to maximize employee compensation, but also reducing insurance cost. The experience modification (MOD) and payrolls are key factors in developing a company’s net rates for workers’ compensation, but average wage per hour represents a big differentiator for most carriers and can lead to even more savings.

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

Wage thresholds have increased consistently in the past decade. This has pushed owners to give sizable raises every few years to maximize employee compensation, but also reducing insurance cost. The experience modification (XMOD) and payrolls are key factors in developing a company’s net rates for workers’ compensation, but average wage per hour represents a big differentiator for most carriers and can lead to even more savings.

Paying your most competent employees above the wage threshold leads to less fraudulent claims, longer tenured employees, and a happier workplace, not to mention the benefit of a drastic cut in net rates for that class code. The gap that is sometimes felt is when there are employees that have the same job description and are earning 30-40% less. Managing payroll inflation is always critical for businesses but let’s think about what this can do to the employees bringing the average pay down for your company. Consider:

More fraudulent claims as the employee has less to lose if they are terminated or laid off;

Resentment toward employees that are doing same job but making more;

Employees are more likely to move to another company to get raises;

Likelihood to miss more time when injured, leading toward higher temporary disability pay which typically can lead to a higher XMOD.

Insurance companies and their underwriters look closely at average salary per employee when they receive a submission with the renewal documentation.

The higher the average pay, the more aggressive they can be with potential scheduled credits in most cases. Obviously, the employer must be selective with who receives a raise and how much but also understand what potentially positive impacts there can be when giving raises in order to hit those thresholds.

And, perhaps just as important is partnering with a broker that specializes in your industry and knows how to properly benchmark you with like organizations. This consistently leads to more productive discussions with underwriters that lead to more scheduled credits. The happier your workforce is, the less claims you tend to see and that translates to long-term savings.

If you have any questions about how you compare to your industry or would like to discuss any other insurance related topic, do not hesitate to reach out to 619-937-0164 or email me directly at ccraig@ranchomesa.com.

How is Payroll Inflation Impacting Your Workers' Compensation Premium?

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

Inflation is rampant everywhere from consumer goods like groceries and gasoline to increased housing costs to labor. Today, I want to talk with you about the specific impact that payroll inflation is having on the workers’ compensation marketplace and ultimately on your premium cost.

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

Inflation is rampant everywhere, from consumer goods like groceries and gasoline to increased housing costs and labor. Today, I want to talk with you about the specific impact that payroll inflation is having on the workers’ compensation marketplace and ultimately on your premium cost.

Any and all businesses have felt the impact of increased payrolls both to retain existing employees and also to attract new ones. For the sake of discussion, let’s use an inflation wage percentage of 6.5%.

On the surface, this 6.5% wage increase is hard enough to manage on profit and loss statements, but below the surface there is also a deeper impact on businesses that for many will catch them unaware.

The two areas I want to talk about are:

The impact the wage increase has on temporary disability claim amounts.

The financial impact that higher wages will have on workers’ compensation carrier P&L’s.

First, temporary disability claim amounts are generally equal to 2/3 of the average weekly earnings of the injured employee. This payment does have a minimum and maximum amount, but for our discussion we will assume the injured worker falls somewhere in between.

So, if the injured worker’s average weekly wage increases by the 6.5%, the disability payment will follow suit. This 6.5% will have several negative impacts. The higher cost of the claim will have a negative impact to the business’ Experience Modification Rate (EMR).

This can be significant to a business since it will not only directly affect the future year’s premium but if the business is a contractor, an elevated EMR can potentially limit pre-qualification approval from many builders.

This is so critical to a business success that here at Rancho Mesa we developed a proprietary Key Performance Indicator (KPI) Dashboard that has the capability to tell our clients the actual claim amount per point of experience modification so they can plan accordingly.

An additional consequence of the claim costs increasing is that a company’s individual loss ratio (claim amounts/premium) with their workers’ compensation carrier will increase. Suffice to say as the loss ratio increases, future premiums will need to increase to offset those higher claim costs. Ideally, to continue to receive the most aggressive pricing, we like to see our clients’ loss ratios stay below 30% so these potential inflation increases need to be understood and addressed proactively.

Shifting gears, let’s look at the impact of payroll inflation on the insurance carrier as a business and what impacts it may have on you the business owner as well.

One of the measurements workers’ compensation carriers look to and monitor for their financial health and well-being is their combined ratio. As a general rule, combined ratios measure dollars collected in premium divided by claims costs and overhead. A good combined ratio indicating a profitable and strong company would be in the low 90%’s.

So, logically speaking, if a carrier is experiencing an increase in temporary disability claims costs and an internal payroll inflation of the same 6.5%, which direction will their combined ratios be going? Obviously, it will be going up, so what are they to do? The most likely choice would be to raise premiums to help offset those increases – unfortunately we know who pays those premium increases.

Now that we understand the impacts that payroll inflation will have on workers’ compensation, what can you do as a business to help mitigate them. The answers are easier than you might think.

This first step is to help reduce the likelihood of claims occurring, thereby reducing the impact of the increase to temporary disability claims on your company.

Conduct a thorough review of your current safety program and look for ways to improve it. How often are you meeting? Are the trainings current and specific to your needs? Is there a tracking system in place where these trainings are documented? At Rancho Mesa, our Client Services Group works closely with our client teams, drawing from our library of over 3,000 specific trainings to help you create meaningful trainings specific to your needs.

Should a claim occur, what are the steps to help mitigate the impact:

Report the claim timely – the quicker your insurance carrier is aware of the claim the better the claim outcome.

Select a carrier that offers “nurse triage” so that in addition to reporting the claim quickly you are able to have an assessment of the injury without going to a clinic and potentially reducing the need for a lost time claim.

If you have implemented all of the above but still have a lost time claim, offer modified work to meet the injuries work restrictions. By offering modified duty, you are able to either pay the injured workers whole salary or a portion of it which eliminates the temporary disability cost from the claim and/or will dramatically reduce the cost. In addition to these claim cost savings, statistics will show when modified duty is offered the potential for litigation is reduced saving even further potential costs.

To create an active and sustainable safety program, look to your trusted advisor (insurance broker) and see what services they have that can assist you.

Do they have a client services team that can provide industry specific trainings, workshops, webinars, certification programs to take your safety program to the next level?

Are you having regular claims meetings with them to review performance, spot trends, look for root causes?

What tools are there to assist you in reviewing your claim data?

Are they able to provide industry benchmarking?

Do they have an in-house workers’ compensation claims advocate to assist you with your open claims to create a better outcome?

Payroll inflation is now a reality and not likely to subside any time soon. As we have shared though, there are proactive steps all businesses can take to help mitigate the impact on your workers’ compensation program today and in the future.

If you are looking for assistance in managing through this or have any additional questions, please reach out to us or email me at dgarcia@ranchomesa.com.

Be informed, be proactive, and implement a plan to make your 2022 the best year ever.

What is the True Cost of a Lost Time Workers’ Compensation Claim?

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

There are many insurance professionals that have tried to quantify the real cost of indemnity or lost time claims, using multipliers anywhere from 2 to 4 times the claim amount in an effort to determine what the real cost of a claim will be to a company. While this may be true, it remains subjective to many. Let me help you understand the ways this type of claim will impact you and then you can decide the real impact to your business.

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

There are many insurance professionals that have tried to quantify the real cost of indemnity or lost time claims, using multipliers anywhere from 2 to 4 times the claim amount in an effort to determine what the real cost of a claim will be to a company. While this may be true, it remains subjective to many. Let me help you understand the ways this type of claim will impact you and then you can decide the real impact to your business.

Let’s assume a claim where the injured worker will be out for 2 to 3 months and the claim’s total incurred amount (which is the combination of paid dollars and reserves) is $50,000. This claim can and will impact your business.

The first direct hit will be your experience modification (X-Mod). While a claim in your current term is delayed a year before going into the calculation, you’ll feel the effects of the remaining 3 years. So, assume the claim is in your 2022-2023 policy year, claims from that year will not go into your 2023-24 policy year but will be in the next three policy terms, 2024-2025, 2025-2026 and 2026-2027.

Each company develops their own “primary threshold,” a term used to describe the maximum incurred loss or cap that any one claim can impact the experience modification. It’s confusing to many policyholders, but this amount regularly changes year-to-year for most companies, as it is derived by the Workers’ Compensation Insurance Rating Bureau (WCIRB) based on the payrolls and class codes a particular business uses and reports.

To simplify this for our clients, we developed a proprietary Key Performance Indicator (KPI) Dashboard that calculates client’s individual Primary Threshold, also detailing how many points to the X-Mod it would add giving them a true indication as to the cost of the claim as it pertains to the X-Mod. Request a personalized KPI for your company.

Now that we understand the impact to the X-Mod, what other areas will be impacted? The next most obvious is the workers compensation carrier’s loss ratio. Adding claim dollars will negatively skew percentages and undoubtedly cause an increase in premium of some amount at renewal.

While the impact to the X-Mod and loss ratio are easy to understand, they are really just the tip of the iceberg. Let’s go below the surface and look at other ways this claim will impact your business.

Losing an employee for any length of time is impactful, but losing the employee for a month or two would likely require the business to fill that person’s job and responsibilities within the company. In many cases this means trying to hire someone new to the organization.

Without going into great detail, the business is likely going to experience additional payroll and benefit costs, training, and likely a decrease in expertise which will most certainly impact the productivity of that particular job.