Industry News

NALP Announces 2017 Safety Award Recipients

Author, Drew Garcia, NALP Program Director, Rancho Mesa Insurance Services, Inc.

Rancho Mesa would like to congratulate all 263 National Association of Landscape Professionals (NALP) members who achieved recognition for their safety efforts in 2017.

Author, Drew Garcia, NALP Program Director, Rancho Mesa Insurance Services, Inc.

Rancho Mesa would like to congratulate all 263 National Association of Landscape Professionals (NALP) members who achieved recognition for their safety efforts in 2017.

"The National Association of Landscape Professionals Safety Recognition Awards Program is designed to reward landscape industry professionals who consistently demonstrate their commitment to safety, and reflects the dedication of these individuals and their companies to creating and maintaining safe work environments," according to the NALP website.

Companies are evaluated in the following categories:

- No vehicle accidents

- No injuries or illness

- No days away from work

We would like to encourage all professional lawn and landscape companies to partake in NALP’s safe company program because participation as a group will continue to evolve and strengthen safety within the industry as whole.

I’m looking forward to supporting the association and these individual achievements in Louisville on October 19th at the annual awards ceremony.

On behalf of Rancho Mesa, congratulations to the participants!

OSHA Announces Top 10 Cited Violations for FY 2017

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

The Occupational Safety and Health Administration (OSHA) released its preliminary top 10 citation list for fiscal year 2017 at the annual National Safety Council (NSC) Congress and Expo, held in late September 2017.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

The Occupational Safety and Health Administration (OSHA) released its preliminary top 10 citation list for fiscal year 2017 at the annual National Safety Council (NSC) Congress and Expo, held in late September 2017.

“One thing I’ve said before in the past on this is, this list doesn’t change too much from year to year,” said Patrick Kapust, deputy director of OSHA’s Directorate of Enforcement and Programs, during the expo presentation. “These things are readily fixable. I encourage folks to use this list and look at your own workplace.”

OSHA compiled the list using data collected from incidents occurring from October 2016 through September 2017.

- Fall Protection in Construction: 6,072 violations.

Frequently violated requirements include unprotected edges and open sides in residential construction and failure to provide fall protection on low-slope roofs - Hazard Communication: 4,176 violations.

Not having a hazard communication program topped the violations, followed by not having or providing access to safety data sheets - Scaffolding: 3,288 violations.

Frequent violations include improper access to surfaces and lack of guardrails - Respiratory Protection: 3,097 violations.

Failure to establish a respiratory protections program topped these violations, followed by failure to provide medical evaluations - Lockout/Tagout: 2,877 violations.

Frequent violations were inadequate worker training and inspections not completed. - Ladders in Construction: 2,241 violations.

Frequent violations include improper use of ladders, damaged ladders and using the top step. - Powered Industrial Trucks: 2,162 violations.

Violations include inadequate worker training and refresher training. - Machine Guarding: 1,933 violations.

Exposure points of operation topped these violations. - Fall Protection-training requirements: 1,523 violations.

Common violations include failure to train workers in identifying fall hazards and proper use of fall protection equipment. - Electrical-wiring methods: 1,405 violations.

Violations of this standard were found in most general industry sectors, including food and beverage, retail and manufacturing

Training materials for each of the items on the OSHA list are available within the Risk Management Center. Contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164, for more information.

3 Steps to Protect Your Employees from San Diego’s Recent Hepatitis A Outbreak

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

Whether you work in the human services sector like healthcare, community outreach, or schools, or you are in the construction industry working in areas like downtown San Diego, your employees may come in contact with the Hepatitis A virus.

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

Whether you work in the human services sector like healthcare, community outreach, or schools, or you are in the construction industry working in areas like downtown San Diego, your employees may come in contact with the Hepatitis A virus (HAV).

As cities throughout San Diego County actively work to stop the spread of the recent Hepatitis A outbreak, some employers are asking how they can protect their employees who may be exposed to the virus.

According to the Center for Disease Control (CDC), the Hepatitis A virus is spread by “person-to-person transmission through the fecal-oral route (i.e., ingestion of something that has been contaminated with the feces of an infected person) is the primary means of HAV transmission in the United States.”

While the local and national media have primarily focused on the concentration of homeless and drug users who have contracted the virus, about 20% of the recent reported cases are not included in that population, according to the “Hepatitis A Outbreak in San Diego, CA” interview by Dennis Stein, linked to on the County of San Diego’s website. However, about half of the 20%, can trace their infection back to working with at risk populations. Thus, the Hepatitis A outbreak should be everyone’s concern, not just those included in the homeless population and drug users.

The “Hepatitis A vaccination is the best way to prevent the disease,” wrote Wilma J. Wooten, Public Health Officer and Director for the County of San Diego Public Health Services, in a letter to emergency responders, businesses, homeless providers and substance abuse treatment providers. While vaccination is an option to prevent infection, good hygiene is also highly effective.

Follow the steps below to help prevent the spread of the Hepatitis A virus to your employees:

1. Wash Hands

First and foremost, instruct employees to frequently wash their hands with soap and warm water after using the restroom, before eating, and after touching handrails, door handles, tools, and other surfaces that are frequently used by others.

Handwashing is “integral to Hepatitis A prevention, given that the virus is transmitted through the fecal–oral route,” according to the CDC’s website.

2. Sanitize

It may be necessary to regularly sanitize your facility or equipment. “Maintain routine and consistent cleaning of bathrooms for employees and the public, using a chlorine-based disinfectant (bleach) with a ratio of 1 and 2/3 cup of bleach to one gallon of water. Due to the high bleach concentration of this mix, rinse surfaces with water after 1 minute of contact time and wear gloves while cleaning,” suggests Wooten.

3. Educate

Awareness and education about the Hepatitis A outbreak is key to preventing the spread of the virus. Based on knowing the facts about how the virus is spread, employees may decide to wear disposable gloves, wash hands more frequently, or change the way they perform their job duties to prevent exposure.

The Risk Management Center provides a variety of training materials to Rancho Mesa clients on Hepatitis A and other bloodborne pathogens. Through online courses, training shorts, videos and other training materials, help educate your employees before there is an infection.

The County of San Diego also provides Hepatitis A information in the form of guidelines, cards, posters, videos and more.

Contact Rancho Mesa Insurance Services at (619) 937-0164 for more information.

Is your Company Prepared for OSHA’s new Silica Rule?

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

On September 23rd 2017 the Occupational Safety and Health Administration’s (OSHA) new silica standard for construction will go into effect. This means contractors who engage in activities that create silica dust or are known in the industry as respirable crystalline silica, must meet a stricter standard for how much dust there workers inhale.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

On September 23rd 2017 the Occupational Safety and Health Administration’s (OSHA) new silica standard for construction will go into effect. This means contractors who engage in activities that create silica dust or are known in the industry as respirable crystalline silica, must meet a stricter standard for how much dust their workers inhale.

What is Crystalline Silica?

Crystalline silica is a common mineral that is found in material that we see every day in roads, buildings and sidewalks. It is a common component of sand, stone, rock, concrete, brick, block and mortar.

What are the Effects?

Exposures to crystalline silica dust occur in common workplace operations involving cutting, sawing, drilling, and crushing of rock, and stone products such as construction tasks and operations using sand products like in glass manufacturing, foundries, sand blasting and hydraulic fracking. Inhaling silica dust can lead to silicosis, an incurable lung disease that can be fatal. Those with too much silica exposure can also develop lung cancer, kidney disease and chronic obstructive pulmonary disease.

What is the New Standard?

The new silica rule lowers the permissible exposure limit from the current standard of 250 micrograms per cubic meter of air to 50 micrograms per cubic meter of air, averaged over an eight hour day, and an action level of 25 micrograms per cubic meter of air.

How will the New Standard protect workers?

The rule significantly reduces the amount of silica dust that workers can be exposed to on the job. That means employers will have to implement controls and work practices that reduce workers exposures to silica dust. For most activities, that means employers will have to ensure the silica dust is wet or vacuumed up before workers can work in the area. Employers are required under the rule to provide training, respiratory protection when controls are not enough to limit exposure and written exposure control plans, measure controls in some cases limit access to high exposure areas. Employers are also required to offer medical exams to highly exposed workers.

How can your company protect itself from Silica Related Claims?

In addition to implementing the necessary controls to protect your employees, we would highly recommend you review your insurance policies to make sure that your company is protected from silica related claims.

Over the last few years, we’ve seen quite a few General Liability carriers putting Silica exclusions on there policies. This isn’t always the case and may be negotiated out depending on the carrier. Another alternative is to obtain a Contractors Pollution Policy that would provide the necessary coverage for this exposure.

Rancho Mesa also recommends taking advantage of the Silica Exposure Training materials available within the Risk Management Center. These materials include an online training course, PowerPoint presentation, training short and quiz in both English and Spanish. Should you have any questions, please contact Rancho Mesa Insurance Services at 619-937-0164.

Workers' Compensation Dual Wage Thresholds Increases for Construction Classes in 2018

Author David J. Garcia, C.R.I.S., A.A.I., President Rancho Mesa Insurance Services, Inc.

In an effort to keep you informed, so that you can begin to plan your 2018 budget, we wanted to let you know of a potential change in the dual wage classes, for many but not all, the dual wage construction class codes.

Author David J. Garcia, C.R.I.S., A.A.I., President Rancho Mesa Insurance Services, Inc.

Updated September 15, 2017 The Workers’ Compensation Insurance Rating Bureau has confirmed the following increases for the 2018 dual wage construction classifications. |

Originally published on May 12, 2017.

In an effort to keep you informed, so that you can begin to plan your 2018 budget, we wanted to let you know of a potential change in the dual wage classes, for many but not all, the dual wage construction class codes.

The Workers’ Compensation Insurance Rating Bureau is proposing increases in the wage threshold for ten different construction industry dual wage classifications and is likely to recommend an increase in an eleventh, by the time it releases its 2018 regulatory filing, next month. The proposed increases range from $1.00 to $2.00 per hour, to keep the thresholds in line with wage inflation. See the chart below for the actual changes.

Dual Wage Thresholds

| Classification | Current Threshold | Recommended Threshold | Threshold Difference | Last Changed |

|---|---|---|---|---|

| 5027/5028 Masonry | $27 | $27 | $0 | 2013 |

| 5190/5140 Electrical Wiring | $30 | $32 | $2 | 2014 |

| 5183/5187 Plumbing | $26 | $26 | $0 | 2014 |

| 5185-5186 Automatic Sprinkler Installation | $27 | $27 | $0 | 2009 |

| 5201-5205 Concrete or Cement Work | $24 | $25 | $1 | 2009 |

| 5403/5432 Carpentry | $30 | $32 | $2 | 2016 |

| 5446/5447 Wallboard Application | $33 | $34 | $1 | 2016 |

| 5467/5470 Glaizers | $31 | $31/further study | $1 | 2016 |

| 5474/5482 Painting/Waterproofing | $24 | $26 | $2 | 2009 |

| 5484/5485 Plastering or Stucco Work | $27 | $29 | $2 | 2014 |

| 5538/5542 Sheet Metal Work | $27 | $27 | $2 | 2009 |

| 5552/5553 Roofing | $23 | $25 | $2 | 2009 |

| 5632/5633 Steel Framing | $30 | $31 | $1 | 2016 |

| 6218/6220 Excavation/Grading/Land Leveling | $30 | $31 | $1 | 2014 |

| 6307/6308 Sewer Construction | $30 | $31 | $2 | 2014 |

| 6315/6316 Water/Gas Mains | $30 | $31 | $2 | 2014 |

Rancho Mesa will keep you informed should the proposed 2018 change go into effect. If you have any questions, please give us a call at (619) 937-0164.

Your Rancho Mesa Team - RM365 Advantage

3 Topics to Discuss with Vendors, Independent Contractors, and Partner Agencies Prior to Working Together

Author, Chase Hixson, Account Executive, Human Services, Rancho Mesa Insurance Services, Inc.

Recently, a non-profit client of mine asked the question: What are the steps I should take with vendors, contracted professionals and partner agencies to make sure my organization is protected should a claim arise as a result of their work? This is a common exposure to many of our clients, and there are several steps that can be taken to protect your business.

Recently, a non-profit client of mine asked the question: What are the steps I should take with vendors, contracted professionals and partner agencies to make sure my organization is protected should a claim arise as a result of their work? This is a common exposure to many of our clients, and there are several steps that can be taken to protect your business.

1. Verify the Proper Insurance is in Place

Any person/organization that you consider working with should be fully insured and able to provide you with a Certificate of Insurance, which lists the coverages, carriers and limits of insurance they have in place. Without their own insurance in place, your company is now assuming full responsibility for anything that may occur as a result of their negligence. Depending on the nature and scope of the work being performed, different types of insurance will be required. An insurance professional can help you determine the specific coverage needed.

Example: A charter school has hired a local animal shelter to bring animals to their students and teach about conservation. One of the animals bites a student. If the animal shelter does not have the proper insurance, the charter school’s insurance will be liable for any action taken against the school.

2. Name Your Business as Additional Insured

In addition to verifying that the correct coverages and limits are in place, you should also require they name your company as an additional insured on their policy. By doing this, your organization will now be indemnified under their policy for claims arising as a result of their work, in which you are named.

Example: In the example where a charter school has hired a local animal shelter to bring animals to their students and one of the animals bites a student, by requiring the animal shelter to name the charter school as an additional insured, the school is covered under the animal shelter’s insurance.

3. Provide a Waiver of Subrogation

A waiver of subrogation means an insured (and their insurance company) are waiving their right to subrogate against another party, should their employee suffer an injury on your premises. Most independent contractors aren’t required to carry insurance, so this wouldn’t apply to them. However, if employees of another company are performing work on your premises, it is wise to have them waive their right to subrogate against your workers’ compensation carrier.

Example: A charter school has hired a local animal shelter to bring animals to their students and teach about conservation. While presenting, an employee of the shelter trips and injures their knee. A waiver of subrogation would void the animal shelter’s workers’ compensation provider from seeking subrogation against the charter school’s workers’ compensation policy. The employee will still be treated, but you won’t suffer the penalty for it.

I strongly recommend reviewing your processes regarding vendor, independent contractors and partner agencies to see what is currently in place. Far too often steps are skipped and businesses are unaware of the liability they are assuming. If you have any question about a specific circumstance, please don’t hesitate to give Rancho Mesa a call at (619) 937-0164, we are happy to assist.

5 Steps to Avoiding Workers’ Compensation Claim Litigation

Author, Jeremy Hoolihan, CRIS, Janitorial Group Leader, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation claims can cost a company time, money, employee productivity, and morale. Litigation is one of the most costly results of a workers’ compensation claim. Once an employee hires an attorney, the time and money it takes for the claim to close drastically increases.

Author, Jeremy Hoolihan, CRIS, Janitorial Group Leader, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation claims can cost a company time, money, employee productivity, and morale. Litigation is one of the most costly results of a workers’ compensation claim. Once an employee hires an attorney, the time and money it takes for the claim to close drastically increases.

There are several reasons why an employee will find the need to hire an attorney. Practicing a sound Risk Management Program can dramatically reduce the likelihood of litigation. Here are some ways you can prevent most workers’ compensation claims from ever reaching that point:

- Acknowledge why employees hire attorneys. The employee/employer relationship is a critical factor in determining if a workers’ compensation claim results in litigation. Employees who feel threatened in some way are more likely to hire an attorney. A few key reasons are:

a. The employee is concerned they will be fired because of the injury and/or ownership or management doesn’t truly feel the injury was work related.

b. The employee feels they will face retaliation for reporting the claim.

c. There is a lack of understanding of the workers’ compensation claim process. For those employees that are faced with a workers’ compensation injury, it can be a very stressful time.

d. There is a fear the claim will be denied or they will be treated unfairly. Attorneys can prey on vulnerable injured employees. Radio and television ads imply injured employees need their assistance in order to get proper treatment and/or a huge settlement they deserve.

- Keep lines of communication open with your employee. Reassure the employee that he or she will have a job when they are able to return to work. In addition, show some compassion and stay in regular contact with the individual. An employee is far more likely to hire an attorney if they are concerned about losing their job or no longer of value to the company.

- Consider the ramifications before firing an injured employee. Termination of an employee after they have been injured on the job can put the company at risk of a lawsuit (Section 132 claim). In addition, terminating an injured worker could cost the company more in wage loss benefits; an injured employee will continue to draw from the workers’ compensation policy if they are unable to return to work, regardless if the company continues to employ them or not. Often, employees are released to modified duty (Return To Work Program). If an employer can accommodate the work restrictions, the employee’s temporary benefits are reduced or eliminated. This can significantly reduce the total cost of the claim.

- Act before a problem employee becomes injured. Once an injury has been reported, it becomes extremely risky to discipline or terminate a problem employee. Address and deal with the employee immediately and be consistent with your documentation.

- Train your supervisors!!!! It is vital that supervisors are trained in reporting and handling claims. They are your first line of defense in preventing claim litigation. Businesses should have a formalized Accident Investigation Program in place. Rancho Mesa provides a Supervisor’s Report of Accident or Near Miss form and a Witness’ Accident Statement form to assist in the investigation process. In addition to all the formal documentation, there are other key strategies a supervisor can use:

a. Do not accuse the injured employee of fraud, even if you know fraud is involved. Supervisors should simply document the facts. If there is suspicion of fraud, make sure you document any supporting evidence in the report and inform the adjuster.

b. Do not negotiate the injured worker’s treatment or return to work schedule. Leave that determination to the claims adjuster.

c. Keep in touch. Instruct the supervisor to check on the injured worker from time to time. Show some compassion and build trust. Assure the employee that their job is secure.

While there is no surefire way to eliminate litigated claims, by following these five steps you should see results. With the average litigated claim costing 30% more than a non-litigated claim, the savings over time could be significant. To discuss implementing this strategy within your company’s Risk Management Program, please contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164.

Assembly Bill 72 Passes to Limit Unexpected Medical Costs to Californians

Effective July 1, 2017, Assembly Bill 72 (Bonta) went into effect by protecting Californians from unexpected medical bills when visiting in-network facilities (i.e., hospitals, labs, and imaging centers). No longer can providers who aren’t contracted with a patient’s health plan step into the operating room, for instance, and charge the patient more than the patient would have expected to pay an in-network provider. Furthermore, the patient can only be billed for his or her in-network cost-share, meaning in-network benefits apply to all providers seen, and services rendered, in an in-network facility.

Effective July 1, 2017, Assembly Bill 72 (Bonta) went into effect by protecting Californians from unexpected medical bills when visiting in-network facilities (i.e., hospitals, labs, and imaging centers). No longer can providers who aren’t contracted with a patient’s health plan step into the operating room, for instance, and charge the patient more than the patient would have expected to pay an in-network provider. Furthermore, the patient can only be billed for his or her in-network cost-share, meaning in-network benefits apply to all providers seen, and services rendered, in an in-network facility.

Over the course of my career, I’ve had to help many clients understand and appeal surprise charges from out-of-network doctors, anesthesiologists, etc., who’ve charged patients separately from the in-network facility, and I have experienced this myself when receiving care. With many/most Preferred Provider Organization (PPO) plans, there is a separate deductible that a member has to satisfy for care received from out-of-network providers, after which, there is less coverage than in-network providers, and the member can be “balance-billed” between what the insurance company pays and what out-of-network providers charge. AB 72 goes a long way toward eliminating such surprise charges.

As always, it’s important to review the Explanations Of Benefits (EOB’s) you receive from your insurance company, to make sure that your benefits have been applied correctly, according to your plan. This is a smart piece of legislation that will help prevent unsuspecting patients in California from getting charged more from out-of-network providers, at least not without prior written consent.

For more information, contact Rancho Mesa at (619) 937-0164.

DHS Alerts OSHA of Possible Electronic Reporting Security Breach

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

On August 1, 2017, the Occupational Safety and Health Administration (OSHA) launched its online electronic data filing application. It was designed to collect and publish injury data on companies throughout the United States in order to comply with a new requirement.

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

On August 1, 2017, the Occupational Safety and Health Administration (OSHA) launched its online electronic data filing application. It was designed to collect and publish injury data on companies throughout the United States in order to comply with a new requirement.

Within just a few weeks of its launch, according to an OSHA spokesperson, the United States Department of Homeland Security’s Computer Emergency Readiness Team alerted OSHA of a possible data breach within the newly launched Injury Tracking Application (ITA).

The warning indicated user information for the tracking application system could have been compromised and the affected company was notified about the apparent breach.

According to a Department of Labor official on August 14, 2017, “Access to the ITA has been temporarily suspended as OSHA works with the system developer to examine the issue to determine the extent of the problem.”

As of today, August 23, 2017, OSHA’s ITA webpage displays an “Alert: Due to technical difficulties with the website, some pages are temporarily unavailable,” preventing anyone from uploading their data.

In an article published by Business Insurance, legal experts were cited as advising companies to wait to file their reports. “I’m not advising anybody to file it before Dec. 1 because it might change,” said Mark Kittaka, a Columbus, Ohio-based partner with Barnes & Thornburg L.L.P. “I don’t know why you’d want to file it early. You may not have to file it all.”

However, Rancho Mesa Insurance Services advises its clients to continue to keep track of their incidents in the Risk Management Center, regardless of what happens with the OSHA electronic reporting requirement. Companies will still need to maintain current OSHA logs, even if the electronic system is unavailable or the electronic reporting requirement changes. If the December 1, 2017 deadline remains in effect, clients will be prepared to submit the data via the Risk Management Center, if the data has been maintained.

Contact Rancho Mesa Insurance Services at (619) 937-0164 if you have questions about how to track your incidents in the Risk Management Center and generate the required OSHA logs.

Surviving an Active Shooter Event: Recognize, React and Prevent Workplace Violence

Author, Sam Brown, Vice President of Human Services Group, Rancho Mesa Insurance Services, Inc.

In the ongoing effort to keep employees safe from workplace violence, it is very important to train workers how to recognize, react to and prevent active shooter events. In most cases, simply having a plan can mean the difference between life and death.

Author, Sam Brown, Vice President of Human Services Group, Rancho Mesa Insurance Services, Inc.

In the ongoing effort to keep employees safe from workplace violence, it is very important to train workers how to recognize, react to and prevent active shooter events. In most cases, simply having a plan can mean the difference between life and death.

PLAN FORMATION

When forming a workplace violence emergency plan, try to answer the following questions:

- How will first observers/responders communicate the threat and to whom?

- How will the threat be communicated to everyone in the facility? Through code words?

- Should the facility be locked down or evacuated?

- Has your security been trained in providing guidance to employees for this type of emergency?

- If your site does not have security, are your workers trained for this type of emergency? Do they know who to call if something happens?

- Do you have site-specific emergency plans in place?

- Do you have the capability to lock down your buildings remotely or deactivate card readers?

PREVENTION

Preventing workplace violence is your first line of defense. Try the following tips to defuse a situation:

- Don't pick fights. Loud and aggressive arguments can easily escalate into physical fights.

- Take verbal threats seriously. Do not aggravate the situation with a threatening response. Report all threats to your supervisor or the company's security department.

- Report any suspicious person or vehicle to security personnel, especially at night. The suspect could be casing the place for a break-in. Or, the person could be stalking an ex-spouse who works with you.

- Also, watch for unauthorized visitors who appear to have legitimate business at your plant. Crimes have been committed by people posing as employees, contractors and repair persons.

- Observe your company's rules prohibiting drugs and alcohol at work. Many violent incidents at work can be traced to the use of these substances.

- Be aware of the neighborhood in which you work and the areas you drive through on your commute. Gang activity and other violence does not always stop at the gate to your plant. Keep to well-traveled and well-lighted areas as you drive to and from work.

- If you drive on the job, don't pick up hitch-hikers. The most important reason for this rule is your personal safety.

- Keep your keys in a secure place so they cannot be stolen or copied. Notify plant security if you have lost your key to the premises.

- Learn how to contact help in an emergency. Speed-dialing numbers should be programmed into phones and emergency numbers should be listed at each phone.

- Some workplaces also have pre-determined code words so one employee can tell another about a dangerous customer or visitor without tipping off the suspect. Learn the distress signals used in your workplace.

- Follow lockup procedures. Wear your identification badge as you are instructed. Never lend your key or entry card to anyone. Keep your entry password a secret by memorizing it instead of writing it down.

TIPS TO SURVIVING A WORKPLACE SHOOTING

RUN: First and foremost, try to escape.

- If there is an escape path, attempt to evacuate.

- Evacuate whether others agree to or not.

- Leave your belongings behind.

- Help others escape if possible.

- Prevent others from entering the area.

- Call 911 when you are safe.

HIDE: If you cannot escape safely, find a place to hide.

- Lock and/or blockade the door.

- Silence your mobile phone.

- Hide behind large objects.

- Remain very quiet.

The hiding place should:

- Be out of the shooter’s view.

- Provide protection if shots are fired in your direction.

- Not trap or restrict your options for movement.

FIGHT: As a last resort, if your life is at risk, act with aggression.

- Attempt to incapacitate the shooter.

- Act with physical aggression.

- Improvise weapons.

- Commit to your actions.

The U.S. Department of Labor Occupational Safety and Health Administration (OSHA) also offers Guidelines for Preventing Workplace Violence for Healthcare and Social Service Workers to help employers prevent such incidents.

For additional resources on Workplace Violence and Active Shooter Preparedness, visit the Rancho Mesa Risk Management Center or contact us at (619) 937-0164.

Congratulations, You’ve Won the Construction Contract – Now, you Need USL&H

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Construction Group

If the title of this article gave you a good chuckle, you most likely have bid a job somewhere near a body of water; then, found out you need U.S. Longshore and Harbor (USL&H) Workers’ Compensation coverage. You were surely not the first one to overlook this requirement and you definitely will not be the last.

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Construction Group

If the title of this article gave you a good chuckle, you most likely have bid a job somewhere near a body of water; then, found out you need U.S. Longshore and Harbor (USL&H) Workers’ Compensation coverage. You were surely not the first one to overlook this requirement and you definitely will not be the last.

History of USL&H

Let’s begin with a USL&H history lesson to understand why it was implemented, nearly 100 years ago.

The U.S. Longshore and Harbor Workers’ Compensation Act was implemented in 1927 to provide compensation to an employee if an injury or death occurred upon navigable waters of the US - including any adjoining pier, wharf, dry dock, terminal, building-way, marine railway or other adjoining area customarily used by an employer in loading, unloading, repairing, dismantling or building a vessel.

The act’s passage compensated maritime workers, including most dock workers and ship builders that were not covered by the Jones Act ( 46 U.S.C. 30004), which only covered seamen, not those who worked in maritime-support industries. Therefore, USL&H workers' compensation was intended to protect those employees who would otherwise not be covered.

Moving forward to present day, to avoid conflict, project owners and general contractors alike require subcontractors and vendors to provide USL&H coverage if projects are close to navigable waters.

Does Every Insurance Carrier Offer USL&H Coverage?

The answer is no. Not every workers' compensation carrier is filed to offer USL&H. Depending on the industry, classification codes and payroll size, there is most likely only a handful of options available. With that said, it’s important to know who those insurance carriers are if you plan on bidding a project that requires USL&H.

Acquiring USL&H Coverage

The first move to acquiring a USL&H policy is to call an insurance representative that has experience in this area. Then, you can develop a game plan that will help you navigate within the USL&H marketplace.

As an eleven-year Best Practices Agency, Rancho Mesa can assist with your USL&H needs. We have been helping clients in the construction field for over 20 years. Contact Rancho Mesa at (619) 937-0164 for more information about this type of policy.

OSHA Launches Electronic Reporting System

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

It is official – the Occupational Safety and Health Administration (OSHA) released its website for the electronic submission of employers’ injury and illness records (i.e., OSHA 300 logs).

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

It is official – the Occupational Safety and Health Administration (OSHA) released its website for the electronic submission of employers’ injury and illness records (i.e., OSHA 300 logs).

After a delay, the Injury Tracking Application website is now available to employers. According the OSHA.gov, “certain employers are required to submit the information from their completed 2016 Form 300A electronically from July 1, 2017 to December 1, 2017.” This means employers have about four months to submit their reports online.

The new requirement was designed to make OSHA records publicly available on the internet in hopes that it would encourage employers to maintain safer working environments.

On the website, employers will be able to manually enter data into a web form, upload a .CSV file, or utilize an automated recordkeeping system with the ability to transmit data electronically via an API (application programming interface).

Rancho Mesa clients who are using the Risk Management Center can expect a .CVS export to be available in October 2017. As long as you have the information in the Risk Management Center, you will be able to generate the .CVS file and upload the reports to the OSHA website.

For those who are not currently using the Risk Management Center to track your incidents, now is a great time to enter the data from 2016, so it is archived in the system and you’ll be able to transfer it once the export is available.

For details regarding who must keep and report OSHA records, visit www.osha.gov/injuryreporting.

5 Tips to Improve Your Fleet and Driver Safety Program

Author, Drew Garcia, NALP Program Director, Rancho Mesa Insurance Services, Inc.

In order to create a best practices fleet safety program that will help you reduce claims and control premiums, we recommend you consider adding the following controls to your written fleet safety program.

Author, Drew Garcia, NALP Program Director, Rancho Mesa Insurance Services, Inc.

In order to create a best practices fleet safety program that will help you reduce claims and control premiums, we recommend you consider adding the following controls to your written fleet safety program.

1. DRIVER SELECTION

- Check MVR’s prior to allowing anyone the opportunity to drive for your company. Enroll drivers into the DMV Pull Program to monitor their driving experience throughout the year.

DMV Pull - Create a short written driver safety quiz that all drivers must pass with a certain percentage of correct answers. Be sure to go over the incorrect answers to help them grow as a safe driver. Consider re-testing on a regular basis.

Quick Safe Driving Quiz, Decision Driving Quiz - Perform a drive test with the employee to make sure they are capable of operating the vehicle safely. Be sure to have employee’s attach trailers, park vehicles with trailers and cone off vehicles if it will be required during the scope of their employment.

Road Test Evaluation Form, Road Test with Trailer Evaluation Form - Create custom policies that outline driving requirements employees must reach to be able to drive for the company and sustain their eligibility to drive.

Sample Driving Requirements

2. FLEET MONITORING SYSTEM

- Consider using fleet management systems to help monitor route efficiency, speed, GPS, and fuel intake while automatically tracking when maintenance is required per vehicle based on individual use. It is highly suggested you disclose that your company uses fleet monitoring systems to all your employees and include this in your employee handbook.

Fleet Monitoring Information

3. DISTRACTED DRIVING POLICY

- Implement and remind employees that distracted driving is the leading cause for motor vehicle accidents. Create a policy that employees are aware of and regularly remind them of your stance on distracted driving.

Sample Distracted Driving Policy, Distracted Driving Quiz, Distracted Driving Article

4. QUICK TRAINING CHECKS AND BALANCES

- Consider creating a proprietary “Company Name Quick 365” safety training techniques to reiterate the importance of safe driving.

- Quick vehicle and rig checks prior to starting the vehicle to ensure everything is secured and ready to be mobile.

- Reward employees for safe driving techniques or suggesting safe company procedures.

- Use actual accidents and incidents to create training topics with possible solutions.

5. DETAILED ACCIDENT INVESTIGATION

- When an accident occurs, be sure your employee is properly trained to document the incident with an in depth accident investigation report.

Accident Investigation Report

For questions about your fleet and driver safety program, contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164

Hired and Non-Owned Liability Coverage: The Sleeping Giant

Author, Daniel Frazee, Vice President, Rancho Mesa Insurance Services, Inc.

Could your company have underlying Auto related exposures that you are not aware of? Let’s assume you have taken several precautions to properly manage the safety of your fleet. But has your management team contemplated potential losses arising from employees operating their own personal vehicles as they relate to your business?

Author, Daniel Frazee, Vice President, Rancho Mesa Insurance Services, Inc.

Could your company have underlying Auto related exposures that you are not aware of? Let’s assume you have taken several precautions to properly manage the safety of your fleet. But has your management team contemplated potential losses arising from employees operating their own personal vehicles as they relate to your business?

Consider the following examples where an employer can be held accountable as a result of actions of your employees using their own vehicles:

- Field employees on the way to or leaving a jobsite

- Administrative employees running errands to the bank, supply store or post office

- An employee runs out to pick up lunch and/or supplies for the team

- An owner or manager decides to rent a vehicle at an out of town conference

- Outside sales reps are provided a car allowance for business use of their personal autos

- A foreman leaves a jobsite and runs to Home Depot for some tools

If an employee in any of these situations is in an at fault accident while driving their own vehicle, the employer can be held responsible for all damages. Typical Auto liability policies only cover employees while they operate company-owned vehicles that are being used for business purposes. Since this coverage does not contemplate nor cover the use of a hired (rented) or non-owned vehicle, a gap in coverage is created. This gap can be filled for a nominal additional premium, by adding hired and non-owned liability coverage. Specifically, these coverages respond when a company is found legally liable for damages after the employee’s personal auto insurance is exhausted. The employee’s personal auto coverage will always be primary to both the employee and the business assuming it was found that the employee at fault while using their vehicle in the course of employment. Without hired and non-owned liability coverage, a company remains exposed to significant costs depending on the degree of bodily and/or physical damage to the vehicle and other parties involved.

Many employers are simply unaware or unwilling to address this ticking time bomb that is non-owned liability. Several “best practice” control measures can be implemented to reduce this exposure:

- Designate a person within the company that will oversee those employees with a non-owned vehicle exposure

- On a bi-annual or annual basis, require employees driving personal vehicles to provide the proof of valid auto insurance

- Consider establishing company mandated minimum limits that are higher than the CA statutory minimum of $15,000/$30,000/$5,000.

- Consider reimbursing employees for any additional premium incurred for increasing limits on their personal policy to reach minimum limits set by the company

- Enroll all employees driving company and/or personal vehicles in the DMV’s employer pull notice program.

In summary, take time to learn more about hired and non-owned liability coverage and how it can impact your bottom line with exposure to severe auto losses. As a National Best Practice Agency 11 years running, Rancho Mesa takes pride in thorough and exacting policy audits that uncover these and many other silent exposures. Through their continually developing Risk Management Center, they offer clients unmatched support with topical safety resources, monthly workshops & trainings, and valuable content.

Contact Rancho Mesa if you have questions about your auto policy.

7 Tips to Protect Your Business from a Fire

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services

As San Diego’s East County battles a series of wild fires, it is a perfect time for business owners to review their insurance policies and proactively manage their fire risk, especially those who are located in semi-rural and rural areas.

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services

As San Diego’s East County battles a series of wild fires, it is a perfect time for business owners to review their insurance policies and proactively manage their fire risk, especially those who are located in semi-rural and rural areas.

Wildfires can quickly turn into structure fires, which can devastate a business. Unfortunately, San Diego County’s fire season has already begun. With scorching temperatures and an abundance of dry brush left over from last year’s rains, this season is particularly dangerous.

In an instant, you can lose everything you have built. Let us make sure you are covered. And, let us help you protect your business with these easy and effective steps:

- Review your insurance policy with your broker.

- Comply with all fire safety codes – we can provide a fire safety company referral, if one is needed.

- Schedule regular landscaping around your building which includes lawns, brush and trees – we would love to introduce you to some of our landscape clients, if you need a referral.

- If a fire threat is issued in your immediate area, run the exterior sprinklers or dampen the building and landscaping with a hose.

- Keep fully charged fire extinguishers on site at all times and have your fire detection and suppression systems tested – we can provide a fire safety company referral, if one is needed.

- Train employees on what to do if there is a fire, including calling 911 and where to access a fire extinguisher – the Risk Management Center has training materials for fire prevention and fire extinguisher use.

- Have a formalized evacuation plan – the Risk Management Center has a great template to help get you started.

These steps are simple and effective ways to help protect your business from fires.

Contact Rancho Mesa with questions about your coverage.

Increase Bonding Capacity Through Jobsite Pictures

Author, Matt Gaynor, Director of Surety Bonding, Rancho Mesa Insurance Services, Inc.

A picture may be worth a thousand words, but it can also be worth hundreds of thousands of dollars when it comes to bonding a new construction project. Let me explain the bonding process and how a few pictures can free up a contractor's bonding capacity.

Author, Matt Gaynor, Director of Surety Bonding, Rancho Mesa Insurance Services, Inc.

A picture may be worth a thousand words, but it can also be worth hundreds of thousands of dollars when it comes to bonding a new construction project. Let me explain the bonding process and how a few pictures can free up a contractor's bonding capacity.

For Construction Bonding Programs, we typically provide a Single Project Limit and an Aggregate Surety Program to guide our clients with pre-approved parameters they can use to bid on projects that require bonding. Although many factors come into play when providing a single project limit, the general rule is 1½ times the largest project completed to date.

The Aggregate Program is made up of the “Cost to Complete” for all bonded and non-bonded projects the contractor has open. To compute the cost to complete, take the estimated cost of the project less the cost to date listed on the work in progress schedule.

One way the agent and bond company can check on the progress of a particular project is by sending a status form to the owner or general contractor. The status form is used to determine how much work has been completed to date. It also includes a comment section to report any problems on the project.

Proving a project is progressing is highly important for a contractor, since it can free up their bonding capacity and allow them to get bonding on additional projects. But, what happens when the owner of a project doesn't return the status form in a timely manner and the contractor needs to free up bonding capacity in order to get bonding on another project?

Case Study

Recently, Rancho Mesa was looking for a way to fit a new bonded project into a contractor’s aggregate program, which was almost at capacity.

In an effort to speed up the process of releasing bonding capacity, the contractor provided pictures (from various angles) of one of his current bonded projects. The pictures showed that several sections of the project were complete. This allowed Rancho Mesa to confirm with the bond underwriter that over 60% of the project was complete. Thus, the underwriter was able to release over $750,000 of capacity to be used on the new project that required bonding.

While the preferred method to release bonding is to get a signed status report from the owner; sometimes, a few pictures from the jobsite can help quicken the process, while we wait for the signed document.

For questions about Surety, contact Rancho Mesa Insurance Services, Inc. at 619) 937-0164.

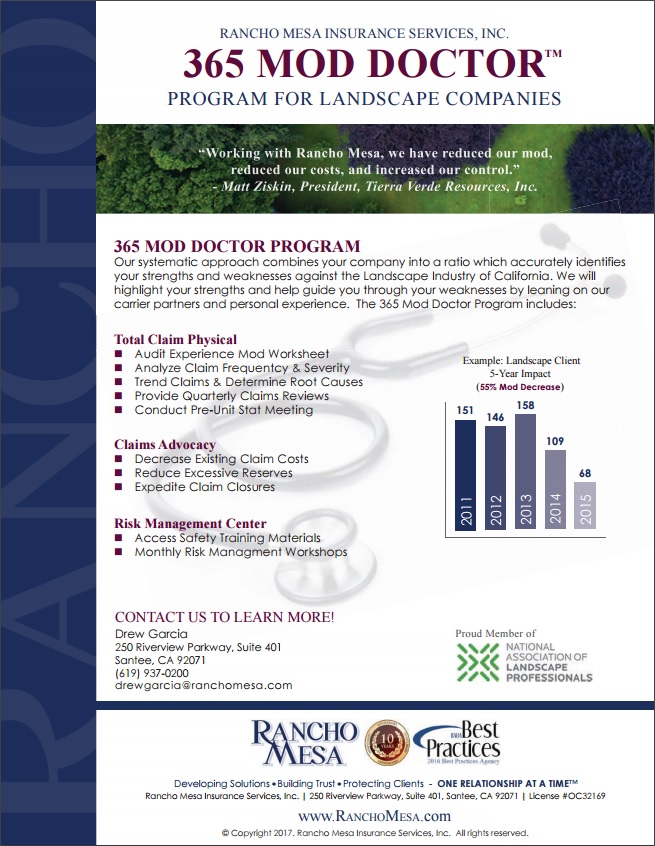

Control your Experience MOD through the MOD Doctor Process.

Author, Drew Garcia, NALP Program Director, Rancho Mesa Insurance Services, Inc.

Successfully maintaining low and predictable workers' compensation costs is a product of establishing a routine that constantly “checks and balances” your all-encompassing insurance program. Our "MOD Doctor" technique lays out a road map so we can guide you throughout the year to gain more control, become more efficient, and ultimately drive down your insurance cost; at no extra expense. What can you expect from this process?

Author, Drew Garcia, NALP Program Director, Rancho Mesa Insurance Services, Inc.

Successfully maintaining low and predictable workers' compensation costs is a product of establishing a routine that constantly “checks and balances” your all-encompassing insurance program. Our MOD Doctor™ technique lays out a road map so we can guide you throughout the year to gain more control, become more efficient, and ultimately drive down your insurance cost; at no extra expense. What can you expect from this process?

Audit Experience MOD Worksheet. Our team analyzes your experience MOD worksheet to ensure the information is accurate with payrolls, claim information, and class codes.

Analyze Claim Frequency, Severity, and Trends. It’s important to analyze your company’s loss information and specifically look for trends in order to prevent further claim activity with similar causes. Furthermore, we compare your loss experience against the landscape industry, in your state, to determine whether you are outperforming or underperforming your industry.

Claims Meetings. The largest companies maintain claim review meetings on a consistent basis. We bring this service to you and adjust the frequency of the meeting to fit your needs. It’s important to have updated information on your open claims, without sacrificing your time or your employee’s time tracking down this data.

Pre-Unit Stat. Your experience MOD is calculated on claims information which is sent into the governing bureau roughly six months into your policy period. Knowing this information, we can accurately project your MOD six months in advance giving you the information you need to begin budgeting for future work,while considering where your insurance cost will be headed.

Claims Advocacy. Our team is your advocate in helping to seek information on your claims, both in the current year and in the past. Our goal through this process is to decrease existing claim costs, reduce excessive reserves, and expedite claim closure, all while considering your unit stat date.

Risk Management Center. We know maintaining up to date and accurate information for tailgate topics, safety procedures, and incident tracking is important. The Risk Management Center streamlines these functions by making them accessible to our clients online.

Contact our Rancho Mesa staff to learn more about how the MOD Doctor can help you control your workers' compensation costs.

Uninsured and Underinsured Motorists Coverage - Are Your Limits Adequate? - Be Careful!

Author, David J. Garcia, A.A.I., CRIS, Rancho Mesa Insurance Services, Inc.

Earlier in the year, we published the article "Commercial Auto Premiums Are Rising - What’s Driving the Increases?," which addresses how insurance companies are all experiencing adverse loss experience within their commercial automobile books of business. The result of these mounting losses is causing a dramatic rise in commercial Auto premiums for most policyholders.

Author, David J. Garcia, A.A.I., CRIS, Rancho Mesa Insurance Services, Inc.

Earlier in the year, we published the article "Commercial Auto Premiums Are Rising - What’s Driving the Increases?," which addresses how insurance companies are all experiencing adverse loss experience within their commercial automobile books of business. The result of these mounting losses is causing a dramatic rise in commercial Auto premiums for most policyholders.

As a result of this trend, we are seeing many carriers and brokers reducing coverage limits and terms on certain lines of automobile coverage. This represents a major concern for any business owner that has any size fleet of vehicles. Reducing limits and/or modifying terms of coverage simply transfers more claim exposure directly to the business owner. And, unfortunately, in many cases, business owners are unaware of the change or ill informed.

One specific line of coverage that we are seeing this occur, and creates great concern, is uninsured/underinsured motorist coverage. The number of uninsured motorists nationwide is alarming and here in California there are between 3.6 million and 4.1 million uninsured drivers, or 14.7 percent of all drivers. Additionally, the minimum limit of insurance in California is only $15,000. So, while many motorists may have insurance, they are woefully “underinsured.” These factors pose potential catastrophic exposures to any business. To illustrate this point, we will briefly define these coverage’s and then look further into how these lower limits of coverage terms may impact the health of your business.

Uninsured Motorists Coverage

Uninsured Motorist Coverage (UM) helps pay your, your employees and your passenger’s medical expenses, lost wages and related property damages if you're in an accident caused by a driver who doesn't have liability insurance.

Underinsured Motorist Coverage

Underinsured Motorist Coverage (UIM) helps pay your, your employees and your passenger’s medical expenses, lost wages, and related property damages, if any of you are hurt in a car accident caused by someone with liability insurance, but whose coverage limits are lower than those you choose for this coverage, and aren't high enough to pay the damages.

Best practices suggests anything less than $1,000,000 limit for uninsured/underinsured coverage is inadequate and puts the business at extreme financial risk. Let me explain by sharing just two, of many real-world, examples of how this could occur. The following examples assume the accident is the fault of an uninsured or underinsured driver:

Example 1. If one of your employees is involved in an automobile accident by either an uninsured or underinsured motorist and it involved the use of a vehicle for business purposes, the resulting medical and indemnity costs would be covered under your company’s workers' compensation policy. Two negative consequences to your overall insurance program develop as a result of this incident. First, your workers' compensation claims experience (loss ratio and EMR) will be negatively impacted. Second, since the “at fault” driver is either uninsured or underinsured, subrogation (or the recovery of the claim dollars from the responsible party) is ruled out as a viable option to your workers' compensation carrier.

Therefore, the auto loss described above would not only negatively affect your auto insurance experience but also your workers' compensation experience, as well. By having a minimum of $1,000,000 UM/UIM limits, you would have allowed you workers' compensation carrier to subrogate the costs of the claim to the auto carrier and thereby reduce the impact to your workers' compensation loss ratio and EMR

Example 2. Let’s assume you have a non-employee in the vehicle and they are involved in an accident involving an uninsured/underinsured motorist and they are injured. Since this is a non-employee, their injuries would not be eligible for coverage under your workers' compensation policy and rest solely on your automobile insurance limits and coverages. Thus, these injuries, once the uninsured/underinsured limit of your automobile policy is exhausted, would become the responsibility of the business. By having a minimum of $1,000,000 UM/UIM limits, you would fill the gap created by the uninsured/underinsured motorist's lack of coverage and protect your business from this catastrophic loss.

These examples have only touched on the medical and indemnity portion of the loss. Consider there may be property damage involved as well, which only further increases the potential of out of pocket expenses a business might be responsible for paying. Additionally, keep in mind that any excess liability policy you may have in place does not cover uninsured/underinsured motorist claims.

In summary we recommend that you review your coverage limits and terms for adequacy concerning these critical coverages. At a minimum, you should have a limit of no less than a $1,000,000 for these coverages. The premium savings by lowering this limit or modifying its coverage terms is insignificant to the catastrophic loss you are exposing your business to. Do not allow one terrible incident to take your business from you when the cost to transfer this risk is marginal.

If you have any questions or need help in accessing your exposures, please call our Rancho Mesa Team. We offer full policy audits as part of our RM365 Advantage Program that helps you to identify any gaps in coverage and provide you with Best Practices risk management recommendations.

OSHA Launches Inaugural Safe + Sound Week

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

The Occupational Safety and Health Administration (OSHA) launched its inaugural Safe + Sound Week, which runs from June 12 - 18, 2017. According to OSHA, Safe + Sound week is "a nationwide event to raise awareness and understanding of the value of safety and health programs that include management leadership, worker participation, and a systematic approach to finding and fixing hazards in workplaces."

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

The Occupational Safety and Health Administration (OSHA) launched its inaugural Safe + Sound Week, which runs from June 12 - 18, 2017. According to OSHA, Safe + Sound week is "a nationwide event to raise awareness and understanding of the value of safety and health programs that include management leadership, worker participation, and a systematic approach to finding and fixing hazards in workplaces."

Why should your company participate?

Workplace safety and health programs can help companies proactively identify and manage workplace hazards before they cause injury or illness. That is good news for companies and employees.

How can businesses participate?

There are three easy steps to participating in Safe + Sound Week. Visit OSHA's Safe + Sound Week webpage for more information on each of these steps:

Step 1: Select the activities you would like to do at your workplace. There are three activities to choose from: Management Leadership, Worker Participation, and Find and Fix Hazards.

Step 2: Plan and promote your events. OSHA has provided Event Tools, Graphics & Signage, Customizable Communications materials, Social Media (#SafeAndSound), and Recruitment Tools.

Step 3: Get recognized for your participation. Complete the online form to generate a Safe + Sound Week Certificate of Recognition and web badge for your organization.

Timely Claim Reporting Lowers Work Comp Claims Costs and Improves Your Bottom Line

Author, David J. Garcia, A.A.I., CRIS, President, Rancho Mesa Insurance Services, Inc.

Studies have shown, by reporting your workers compensation claims in a timely basis, not only will your injured employee receive better medical treatment, it will boost company morale. Both the injured worker, as well as other employees, will see your sincere concern for their wellbeing. In addition, timely reporting practices will also improve your risk profile through reducing the overall cost of the claim, which leads to lower loss ratios and lower experience modifiers, thus, resulting in lower premiums and improvement in your bottom line.

Author, David J. Garcia, A.A.I., CRIS, President, Rancho Mesa Insurance Services, Inc.

Studies have shown, by reporting your workers compensation claims in a timely basis, not only will your injured employee receive better medical treatment, it will boost company morale. Both the injured worker, as well as other employees, will see your sincere concern for their wellbeing. In addition, timely reporting practices will also improve your risk profile through reducing the overall cost of the claim, which leads to lower loss ratios and lower experience modifiers, thus, resulting in lower premiums and improvement in your bottom line.

The following are four areas that support the early and timely reporting of claims:

- Manage Claims More Efficiently Reporting a claim quickly allows the claims examiner:

- To determine whether or not the claim is compensable.

- To meet state regulations that prohibit denial of claims after a specified time period.

- To secure appropriate treatment for the injured worker.

- To conduct an investigation and determine if fraud is suspected.

- To receive timely witness statements and pictures of the incident.

- Keep The Claim Costs Down – Improve Loss Ratio – Improve Experience Modifier Delayed reporting can significantly increase workers’ compensation claim costs, according the National Council on Compensation Insurance.

- Claims reported after 2 weeks of occurrence are 18% more expensive than those reported within 1 week of occurrence.

- Claims reported after 3-4 weeks of occurrence are 30% more expensive than those reported within 1 week of occurrence.

- Claims reported 1 month of occurrence are 45% more expensive than those reported within 1 week of occurrence.

- Most significantly, back injuries, as a group, are 35% more expensive if not reported within the first 7 days post-injury.

- Reduce Litigated Claims

- 47% of all claims reported after 4 weeks become litigated, which on average increase claims costs by 30%.

Source: NCCI’s Detailed Claim Information data for Report Years 2010 and 2011 case incurred losses valued as of 18 months after report date; not developed to ultimate - Close Claims Faster

- 50% of claims that are reported within the first two weeks close within 18 months.

- Only 29% of claims that are reported more than a month after the accident close within the same timeframe.

Source: NCCI’s Detailed Claim Information data for Report Years 2010 and 2011 case incurred losses valued as of 18 months after report date; not developed to ultimate.

| Reporting (Lag) Time | Expense Increase |

|---|---|

| 2 Weeks | 18% |

| 3 Weeks | 29% |

| 4 Weeks | 31% |

| 4 Weeks | 31% |

| 5 Weeks | 45% |

If you’re not currently reporting your claims timely, we strongly encourage you to adopt this “Best Practice” and make it a part of your company’s overall risk management program. Reporting your claims on a timely basis will get your injured employee the proper treatment quicker, provide your carrier the controls they need to manage the claim effectively, improve your risk profile, and lower your insurance costs.