Industry News

Work Comp Unit Stat: The Meeting That Saves You Money

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

California business owners are aware that their experience modifier (XMOD) is published annually, roughly three to four months before the expiration of their current workers compensation policy term. However, more often than not, companies are missing an incredible opportunity to make an impact on the calculation of their XMOD by strategically evaluating their work comp claims prior to the most critical month in the XMOD calendar known as Unit Stat.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

California business owners are aware that their experience modifier (XMOD) is published annually, roughly three to four months before the expiration of their current workers compensation policy term. However, more often than not, companies are missing an incredible opportunity to make an impact on the calculation of their XMOD by strategically evaluating their work comp claims prior to the most critical month in the XMOD calendar known as Unit Stat.

The Workers’ Compensation Insurance Rating Bureau (WCIRB) defines the process of receiving loss and payroll information by classification as the Unit Statistical Report. The information is reported to the WCIRB by insurance carriers at specific intervals based on your company’s policy effective date. The information is valued for the first time 18 months after the inception of your policy and every 12 months thereafter.

A policy that incepts in January 2020 will be valued for the first time in July of 2021 (18 month mark). This information will remain in your XMOD calculation for the valuations at 30 months and 42 months.

Once this information has been received by the WCIRB, from the respective carriers, it cannot be altered or changed until the following year’s unit stat. Thus, you may have a positive outcome on an existing open claim (reserve reduction or closure) but not see the benefit until the following year. Revisions to the XMOD once published are limited to a few circumstances; more information about revisions can be found here.

The loss information, sent to the WCIRB from the insurance carriers, will be evaluated at the paid (closed claim) or reserved (open claim) amounts. Typically, a claim that has been open for longer than 18 months signifies severity, litigation, lost time, permanent disability, or a combination of the group. For this reason it is absolutely critical that as a part of your risk management process you execute a

pre-unit stat meeting.

When should I schedule my Unit Stat meeting?

What should I do at this meeting?

Who needs to be involved?

How will this meeting save me money?

As a client of Rancho Mesa, we build this meeting into your annual service plan and take care of engaging the parties who need to be involved for the betterment of your XMOD.

Ready to learn more about Unit Stat? Join us for a complimentary 25-minute webinar where we will discuss the process in greater detail and take time for Q&A.

Still not sure if further learning is necessary, ask yourself these questions:

Have you ever been surprised by your XMOD being higher than you would have thought?

Have you ever had an XMOD above 1.00?

Has your XMOD ever caused your premium to increase?

The webinar can be viewed on-demand by clicking the link below.

California Workers’ Compensation Dual Wage Thresholds Increases Approved for Construction Classes in 2020 – Bottom Line Hit Hard

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

In an effort to keep you informed, so that you can begin to budget for 2020, we wanted to let you know of the approved changes in the dual wage classifications effective January 1, 2020.

Originally published May 23, 2019.

Updated September 19, 2019.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

In an effort to keep you informed, so you can begin budgeting for 2020, we want to let you know of the approved changes in the dual wage classifications effective January 1, 2020.

The increases range from $1.00 to $3.00 per hour, to keep the thresholds in line with inflation. However these changes will have an immediate effect on your bottom line.

In the classes of business that are facing a $3 increase, this equates to a low of 9.3% to a high of 10.3%. See the chart below for the actual approved changes. Not only does this have an impact on wages, payroll taxes, and your bottom line, it may also have an impact on your workers compensation premiums. If you find yourself in a situation where the wage increase is not practical, this will push those employees into the under classification which will have a substantially higher workers compensation rate. In either case, proactive planning will be required so you’re not caught unprepared.

Following are the individual classes and approved changes:

Dual Wage Thresholds

| Classification | Current Threshold | 2020 Threshold | Threshold Difference | Last Changed |

|---|---|---|---|---|

| 5027/5028 Masonry | $27 | $28 | $1 | 2013 |

| 5190/5140 Electrical | $32 | $32 | $0 | 2018 |

| 5183/5187 Plumbing/Heating/Refrigeration | $26 | $28 | $2 | 2014 |

| 5185-5186 Fire Sprinkler | $27 | $29 | $2 | 2009 |

| 5201-5205 Concrete or Cement Work | $25 | $28 | $3 | 2018 |

| 5403/5432 Carpentry | $32 | $35 | $3 | 2018 |

| 5446/5447 Wallboard Application | $34 | $36 | $2 | 2018 |

| 5467/5470 Glaizers | $32 | $33 | $1 | 2019 |

| 5474/5482 Painting/Waterproofing | $26 | $28 | $2 | 2018 |

| 5484/5485 Plastering or Stucco Work | $29 | $32 | $3 | 2018 |

| 5538/5542 Sheet Metal Work | $27 | $27 | $0 | 2014 |

| 5552/5553 Roofing | $25 | $27 | $2 | 2018 |

| 5632/5633 Steel Framing | $32 | $35 | $3 | 2018 |

| 6218/6220 Excavation/Grading | $31 | $34 | $3 | 2018 |

| 6307/6308 Sewer Construction | $31 | $34 | $3 | 2018 |

| 6315/6316 Water/Gas Mains | $31 | $34 | $3 | 2018 |

In an effort to help control workers compensation costs, we have developed several proprietary programs including the RM365 Advantage Safety Star Program™ and RM365 StatTrac™ that can help control these increases. Please reach out to me at sclayton@ranchomesa.com to ask any questions about the above or to learn more about our proprietary programs.

Painters Stretching Can Lead to Reduced Premiums

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

Having played professional baseball for several years, I know the importance of stretching to prepare oneself for the day. My team would stretch when we got to the field, then again before batting practice, and once more before the game started. Most people reserve stretching for sporting events. They forget the importance of stretching before work - feeling they will “loosen up” as the day goes along. However, there are countless ways for employees to become injured and those medical bills can grow all too fast.

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

Having played professional baseball for several years, I know the importance of stretching to prepare oneself for the day. My team would stretch when we got to the field, then again before batting practice, and once more before the game started. Most people reserve stretching for sporting events. They forget the importance of stretching before work — feeling they will “loosen up” as the day goes along. However, there are countless ways for employees to become injured and those medical bills can grow all too fast.

While there are things that can be done to try to mitigate the claims after they occur, the best way to save on your premium is to prevent injuries from ever happening. If you can set aside just 5 minutes a day for your employees to stretch their muscles that will be used throughout the day, that could reduce strain and pull claims dramatically.

As recent as 2015, the WCIRB has broken down the most common injuries that occur in the 5474/5482 class codes. 57% of the injuries could have possibly been prevented by allotting just a few minutes a day for stretch and wellness. The most common injuries for painters are to their lower extremities, back, and upper extremities (not including the hand). It is easy to see, that with all the bending down and painting above their heads, cumulative injuries are going to happen if no precautions are taken. An average claim for these types of injuries can cost just shy of $35,000. Having multiple claims of these types can be crippling for a company.

Having employees stretch when they get to the jobsite, and after lunch is the best way to reduce soft tissue claims. Making sure the legs are ready to bend, the back and neck are stretched out, and shoulders are prepared for the work at hand, is as important as anything they will be doing that day.

Your employees may need a little extra energy in the morning, but caffeine reduces blood circulation and can lead to stiffness when returning from lunch. It is important to get the blood flowing again with some trunk twists, toe touches, and arm swings. This will increase blood flow throughout the body. Finally, inflammation can worsen as the day progresses, and having leafy greens reduces inflammation. Providing a healthy lunch can help to build morale and keep that nagging soreness away while increasing productivity.

Rancho Mesa has put together a Mobility and Stretch Program™ for their clients. The program has reduced the number of reported strain and pull claims, and has significantly helped drop clients’ MODs. Please reach out to Rancho Mesa Insurance Services, Inc. with any questions you may have.

The Ticking Time Bomb for Plumbing and Mechanical Contractors: Lower Expected Loss Rates Can Mean Higher Experience Modifications

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Insurance Services, Inc.

The Workers Compensation Insurance Rating Bureau (WCIRB) released the 2019 Expected Loss Rates (ELR’s) in the 4th quarter of 2018. The ELR’s in the plumbing class code 5187 dropped 17% on January 1st 2019. This decrease is not getting significant attention, but could potentially create negative implications for California plumbing contractors and their respective experience modifications in 2019, 2020 and beyond.

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Insurance Services, Inc.

The Workers Compensation Insurance Rating Bureau (WCIRB) released the 2019 Expected Loss Rates (ELRs) in the 4th quarter of 2018. ELRs are the average rate at which losses for a classification are estimated to occur during an experience rating period. They are generally expressed as a ratio per $100 of payroll and can often have a dramatic impact on experience modifications. To support this point, the ELRs in the plumbing class code 5187 dropped 17% on January 1, 2019. This decrease is not getting significant attention, but could potentially create negative implications for California plumbing contractors and their respective experience modifications in 2019, 2020, and beyond. All plumbing and mechanical contractors should be made aware so they can prepare and make changes to protect themselves from the impact. Similar to a leak behind a wall, this could go undetected until the experience mods are released and then it is too late and too much damage has been done.

LINKING ELRs WITH YOUR PRIMARY THRESHOLD

The lowered expected loss rates also impact primary thresholds. Your primary threshold is the maximum primary loss value for each individual worker’s compensation claim. If primary thresholds move lower, one small lost time claim can cause a significant spike in an experience modification. An elevated experience modification can impact not only pricing, but opportunities to bid certain types of work within the commercial sector.

WHAT CAN YOU DO TO GET OUT IN FRONT OF THIS?

If these terms are completely new to you and your organization, lean on your insurance broker to provide the education needed to get up to speed. That can start with building a detailed service plan that focuses on controlling your experience modification. Some examples of critical elements that should be discussed would include:

Addressing open reserves on claims that are impacting the future experience modification.

How the timing of the unit stat filing will affect the future experience mod and cost.

Ensuring that your safety program addresses the root cause of claim frequency and severity.

Trainings that are aligned with OSHA compliance.

Experience MOD forecasting up to 7 months prior to your firm’s effective date.

AVOIDING THE TICKING TIME BOMB

The ticking time bomb can be avoided by taking certain steps and actions that are strategically put in place with your insurance broker. If this article has created concern and/or these terms are brand new to you, pick up the phone and schedule an experience modification control meeting with an advisor from Rancho Mesa at (619) 937-0164. Their Best Practices approach to managing risk starts with a client-centric process that is focused on education and execution.

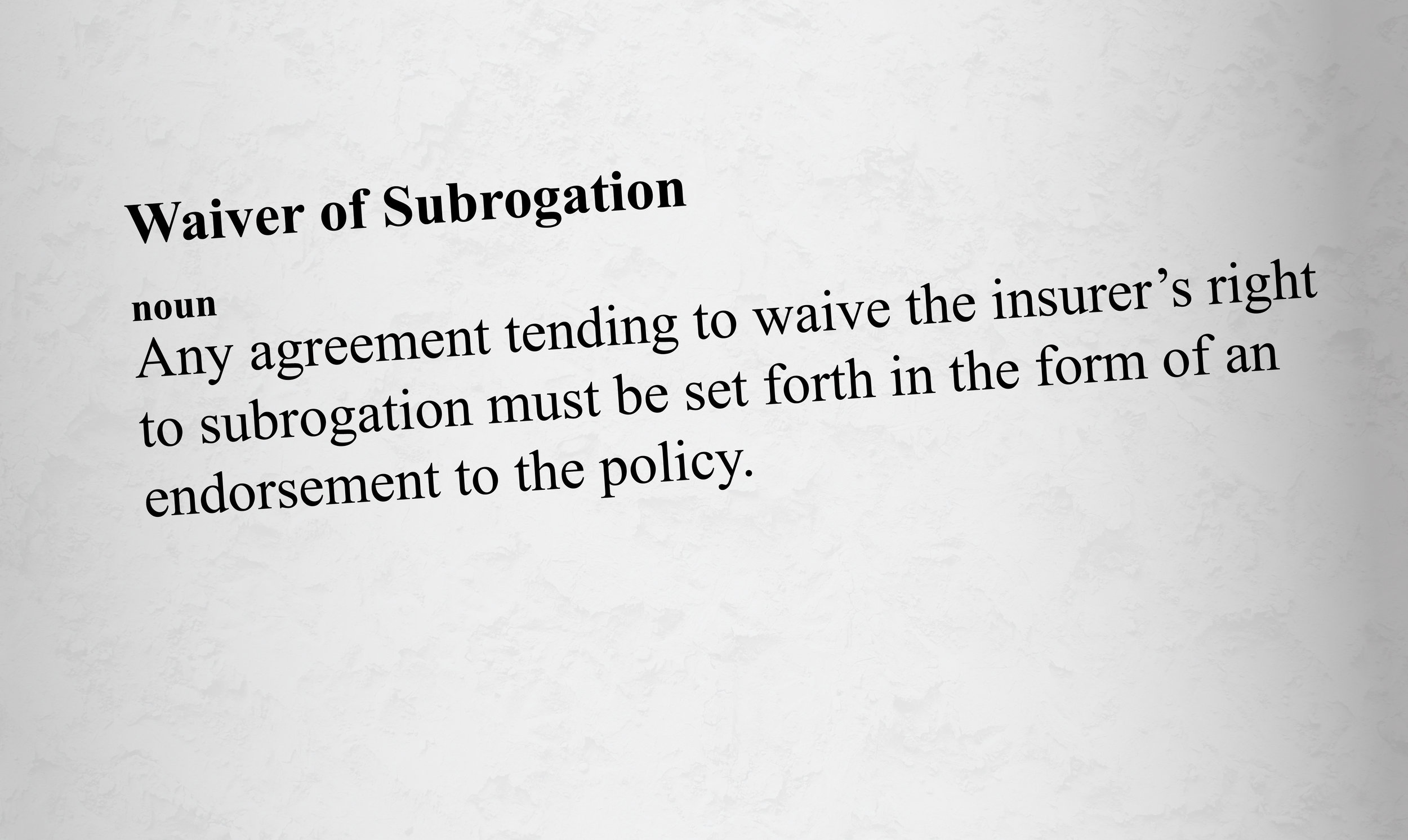

Understanding Waivers of Subrogation for Contractors

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

In an era where general contractors commonly require a Waiver of Subrogation from its sub-contractors before they are allowed to step foot on the jobsite, it is important to understand how a Waiver of Subrogation functions. Most companies simply tell their agent they need the waiver added to their contract, but what does this mean? How does it affect the policy?

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

In an era where general contractors commonly require a Waiver of Subrogation from its sub-contractors before they are allowed to step foot on the jobsite, it is important to understand how a Waiver of Subrogation functions. Most companies simply tell their agent they need the waiver added to their policy, but what does this mean? How does it affect the policy?

Subrogration is "the legal process by which an insurance company, after paying for a loss, seeks to recover all or a portion of the loss from another party who is legally wholly or partially liable for that loss," according to the Workers' Compensation Insurance Rating Bureau of California (WCIRB). So, a Waiver of Subrogration prevents your insurance carrier from recovering funds paid on a claim from the named party requesting the waiver.

When subrogating, three things must be established:

1) The defendant was negligent (or that a product was defective),

2) Negligence proximately caused the damages for which the carrier paid, and

3) The amount and nature of the damages.

If you cannot establish any one of these three, there will be no subrogation.

Subrogation is used throughout various lines of insurance. It is very common in dealing with auto insurance claims. If you are in an accident and the other driver is deemed to be at fault, your insurance company will respond first by paying to have your vehicle fixed. Then, the carrier will collect from the at fault driver’s insurance company to recover the amount they had to pay to fix your car. The insured’s carrier jumps on the claim immediately so that the insured will not have to wait for the claim to be disputed and resolved before their car is repaired. Claims are handled the same for every line of insurance, unless there is a Waiver of Subrogation in place.

When a sub-contractor is hired and has signed a Waiver of Subrogation for the project owner or general contractor, they are essentially waiving their carrier's ability to recover the money that was paid out on a claim that was caused by a third party's negligence. Waivers of subrogation often come in two formats. Either, the waiver specifically names an entity that the carrier waives its’ right to subrogate against, or a Blanket Waiver of Subrogation. If a Blanket Waiver of Subrogation is provided, the carrier must obtain permission from the named insured to subrogate against a third party.

When adding a Blanket Waiver of Subrogation to a policy, there is an additional fee to offset the carrier’s ability to reclaim money from any losses that were caused by a third party's negligence. These fees can change from carrier to carrier and it is a good move to review each policy to know exactly what you are paying for waivers. Adding a blanket waiver of insurance does not increase coverage or limits, it simply absolves an owner/general contractor of their liability.

With Waivers of Subrogation becoming more prevalent, it is easy to see how important it is as a business owner to know exactly what is covered and what you are waiving.

If you have any questions or would like to understand subrogation further, please contact Rancho Mesa at (619) 937-0164.

Update: 8868 Class Code Changes - Proposed WCIRB Changes Awaiting Public Hearing August 3rd

Author, Chase Hixson, Account Executive, Human Services Group, Rancho Mesa Insurance Services, Inc.

On August 3, 2018, the California Department of Insurance will hold a public hearing regarding the proposed changes to the 8868 Class Codes.

On August 3, 2018, the California Department of Insurance will hold a public hearing regarding the proposed changes to the 8868 Class Codes.

The proposed changes, at the recommendation of the Workers’ Compensation Insurance Rating Bureau (WCIRB), will break the 8868 class code into the following divisions:

8868 & 9101 – K-College Schools (Academic Professionals & Non-Academic Professionals, Respectively)

8869 & 9102 – Vocational Schools, Academic Professionals & Non-Academic Professionals respectively)

8871 – Supplemental Education

8872 – Social Services

8873 – Training or Day Programs for Adults

8874 – Special Education Services for Children & Youth

8876 – Community Based Adult Services

These changes, if approved, could have a significant impact on California businesses. A recent article by the Workers’ Compensation Executer, a leading news source in the insurance industry, suggest up to 25% increases in some of the proposed class codes.

Rancho Mesa has specialized in the education arena for nearly 20 years and is prepared to assist clients with this transition. If you have any questions, please contact Rancho Mesa Insurance Services at (619) 937-0164.

Six Reasons a Company’s Experience Modification Could be Recalculated

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation costs continue to be one of the most costly expenses for business owners in California. With recent reform, California has maintained steady rate decreases in the workers’ compensation marketplace. Unfortunately California still maintains some of the highest rates in the country, often times two to three times the nations average.

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation costs continue to be one of the most costly expenses for business owners in California. With recent reform, California has maintained steady rate decreases in the workers’ compensation marketplace. Unfortunately, California still maintains some of the highest rates in the country, often times two to three times the nations average.

Controlling insurance costs is vital to staying profitable and often times, staying in business. An important way business owners can control their insurance costs is by controlling their Experience Modification or X-MOD. An X-MOD is a benchmark of an individual employer against others in its industry, based on that employer's historical claim experience. This comparison is expressed as a percentage which is applied to an employer's workers' compensation premium.

The premium impact of a credit X-MOD (less than 1) vs a debit X-MOD (more than 1) can be significant. Business owners budget around their insurance costs. When there are unforeseen changes to their insurance costs it can have a dramatic effect. While it is rare, there are situations when an X-MOD can change in the middle of a policy term. Below are six circumstances when this could happen:

- If a claim that has been used in an X-MOD calculation is subsequently reported as closed mid policy term AND closed for less than 60% of the aggregate of the highest value, then the X-MOD is eligible for recalculation.

- In cases where loss values are included or excluded through mistake other than error of judgement. Basically, this rule takes into consideration the element of human error.

- Where a claim is determined non-compensable. Meaning the injury was determined to be non-work related.

- Where the insurance company has received a subrogation recovery or a portion of the claim cost is declared fraudulent.

- Where a closed death claim has been compromised over the sole issue of applicability of the workers’ compensation laws of California. Basically, if a person passes away at work but it was determined that the person had a pre-existing condition which caused the death, not work itself.

- Where a claim has been determined to be a joint coverage claim. This occurs mainly with cumulative trauma claims where there was no specific incident that caused an injury, but an injury that developed over time (i.e., wear and tear).

If any of the circumstances above have occurred, than a revised reporting shall be filed with the Workers’ Compensation Insurance Rating Bureau (WCIRB) and it shall be used to adjust the current and two immediately preceding experience ratings.

If you would like to discuss this topic in further detail, and learn how Rancho Mesa Insurance can audit your X-MOD worksheet for potential recalculations, please contact us at (619) 937-0164.

Workers' Compensation Dual Wage Thresholds Increases for Construction Classes in 2018

Author David J. Garcia, C.R.I.S., A.A.I., President Rancho Mesa Insurance Services, Inc.

In an effort to keep you informed, so that you can begin to plan your 2018 budget, we wanted to let you know of a potential change in the dual wage classes, for many but not all, the dual wage construction class codes.

Author David J. Garcia, C.R.I.S., A.A.I., President Rancho Mesa Insurance Services, Inc.

Updated September 15, 2017 The Workers’ Compensation Insurance Rating Bureau has confirmed the following increases for the 2018 dual wage construction classifications. |

Originally published on May 12, 2017.

In an effort to keep you informed, so that you can begin to plan your 2018 budget, we wanted to let you know of a potential change in the dual wage classes, for many but not all, the dual wage construction class codes.

The Workers’ Compensation Insurance Rating Bureau is proposing increases in the wage threshold for ten different construction industry dual wage classifications and is likely to recommend an increase in an eleventh, by the time it releases its 2018 regulatory filing, next month. The proposed increases range from $1.00 to $2.00 per hour, to keep the thresholds in line with wage inflation. See the chart below for the actual changes.

Dual Wage Thresholds

| Classification | Current Threshold | Recommended Threshold | Threshold Difference | Last Changed |

|---|---|---|---|---|

| 5027/5028 Masonry | $27 | $27 | $0 | 2013 |

| 5190/5140 Electrical Wiring | $30 | $32 | $2 | 2014 |

| 5183/5187 Plumbing | $26 | $26 | $0 | 2014 |

| 5185-5186 Automatic Sprinkler Installation | $27 | $27 | $0 | 2009 |

| 5201-5205 Concrete or Cement Work | $24 | $25 | $1 | 2009 |

| 5403/5432 Carpentry | $30 | $32 | $2 | 2016 |

| 5446/5447 Wallboard Application | $33 | $34 | $1 | 2016 |

| 5467/5470 Glaizers | $31 | $31/further study | $1 | 2016 |

| 5474/5482 Painting/Waterproofing | $24 | $26 | $2 | 2009 |

| 5484/5485 Plastering or Stucco Work | $27 | $29 | $2 | 2014 |

| 5538/5542 Sheet Metal Work | $27 | $27 | $2 | 2009 |

| 5552/5553 Roofing | $23 | $25 | $2 | 2009 |

| 5632/5633 Steel Framing | $30 | $31 | $1 | 2016 |

| 6218/6220 Excavation/Grading/Land Leveling | $30 | $31 | $1 | 2014 |

| 6307/6308 Sewer Construction | $30 | $31 | $2 | 2014 |

| 6315/6316 Water/Gas Mains | $30 | $31 | $2 | 2014 |

Rancho Mesa will keep you informed should the proposed 2018 change go into effect. If you have any questions, please give us a call at (619) 937-0164.

Your Rancho Mesa Team - RM365 Advantage