Industry News

Leveraging Your Experience Modification Rating to Your Advantage

Author, Matt Gorham, Account executive, Rancho Mesa Insurance Services, Inc.

Your Experience Modification Rating (e.g., EMR, X-Mod, or Mod) can have a significant impact on controlling costs within your insurance program. While most business owners recognize that a lower EMR typically leads to lower insurance costs, few owners understand the mechanics for determining an EMR and how they can be used to proactively manage resources to their company’s benefit.

Author, Matt Gorham, Account executive, Rancho Mesa Insurance Services, Inc.

Your Experience Modification Rating (e.g., EMR, X-Mod, or Mod) can have a significant impact on controlling costs within your insurance program. While most business owners recognize that a lower EMR typically leads to lower insurance costs, few owners understand the mechanics for determining an EMR and how they can be used to proactively manage resources to their company’s benefit.

An EMR is determined by evaluating a company’s recent history of payrolls and job related injuries, relative to its own industry, to benchmark them to their peer group.

If a company’s incurred losses (both paid and reserved) exceed the average within its industry, it will result in a debit mod (i.e., EMRs above 100) which leads to higher premiums. If the incurred losses are less than the industry average, the company will earn a credit mod (i.e., EMRs under 100) resulting in lower premiums.

As your EMR changes from year to year, it will directly increase or decrease your company’s workers’ compensation premiums, thus impacting overhead costs. Higher EMRs will increase overhead costs and can lead to increased bid costs, reduced profit margins, and in some cases restrict you in the pre-qualification process.

In the construction world, passing higher costs on to your customers in a competitive bidding process can prevent you from securing contracts. Choosing instead to absorb those additional costs, however, can jeopardize your company’s growth, financial stability, or possibly stop you from having the funds necessary to complete the job.

But managing your EMR is more than simply having the good fortune to avoid expensive claims. It is important to recognize that not all claims impact your EMR the same. Severity and frequency of claims both play an important role in your EMR, as does your primary threshold.

Using these key data points, we are able to create a proprietary KPI dashboard for clients providing valuable insights to the mechanics of their EMR. Business owners are able to see their:

Primary Threshold and Maximum EMR Impact

Claim Dollars Equal to 1 Point of EMR

Maximum Controllable Points within the EMR

Individual Frequency Trends and Benchmarking to Industry

Individual Severity Trends and Benchmarking to Industry

Lowest Possible EMR

Projected EMR

Our KPI dashboard has become a must have tool for business owners, providing a better understanding of how to manage their EMR, allowing them to more reliably forecast overhead costs, and proactively address safety concerns. Coupled with Rancho Mesa’s in-house workers’ compensation claims advocate, business owners can more efficiently deploy resources and return-to-work programs to mitigate claim costs.

To request your own KPI dashboard and start putting it to use within your business, contact me at (619) 486-6554 or mgorham@ranchomesa.com.

How Important is Your EMR in the Pre-Qualification Process?

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

With 2024 right around the corner, general engineering and trade contractors will be required by government agencies and general contractors to enter the annual pre-qualification process in order to bid work. These entities are looking closely at a company’s project history, including project size, bonding capacity, limits of insurance as well as a companies’ Experience Modification Rate (EMR).

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

With 2024 right around the corner, general engineering and trade contractors will be required by government agencies and general contractors to enter the annual pre-qualification process in order to bid work. These entities are looking closely at a company’s project history, including project size, bonding capacity, limits of insurance as well as a companies’ Experience Modification Rate (EMR).

An EMR is a numeric representation of a company’s audited payrolls for the three prior years (not including the current year) and your workers’ compensation claims history, compared to businesses in the same industry or standard classification. EMR’s create a baseline for business while allowing for a surcharge or debit when employers claims are worse than expected and a credit when employer’s claims are better than industry average. Companies with and EMR rate below a 1.00 are considered better than average, while greater than 1.00 are consider below average.

Pre-Qualification Process

In the highly competitive environment of construction bidding, it has become common that government agencies and general contractors will preclude contractors from the pre-qualification process if your EMR exceeds 1.00 or 1.25. In my opinion, this represent an oversight as many companies have strong will developed safety programs, yet their EMR is holding them back. Some examples of this include:

The EMR is a lagging factor. Only the last three policy periods, not including the current policy period are taken into consideration for the calculation.

EMR’s can include claims that may have been unavoidable and don’t represent a lack of safety (i.e. an employee was involved in an auto accident and was not at fault).

Large indemnity claims can have a significantly higher impact for a smaller company vs. a larger company with a similar size claim.

Rather than placing such critical importance on the contractors current EMR, government agencies and general contractors designing the pre-qualification process should include frequency indicators like incident and DART Rate (i.e. days away, restricted or transferred) or put more emphasis on a contractors’ 5 or 10-year average EMR.

Given the importance of the pre-qualification process an and the potential for contractors to be precluded from new opportunities to bid work, we’ve developed a proprietary Key Performance Indicator “KPI” Dashboard as well as our SafetyOne Desktop & Mobile App to assist companies in managing their EMR. These tools will, among many things, help you:

Benchmark your experience against your peers.

Weigh the impact of any claim to your EMR.

Project your future EMR a year in advance.

If you would like a KPI created for your company, or would like to learn more about our SafetyOne App, please email me at sclayton@ranchomesa.com.

Implementing Best Practices when Hiring in the Construction Industry

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

With unemployment rates settling near 4 percent, it is becoming increasingly difficult to find the right employees to help grow your construction company. With most able-bodied workers having secure employment, this leads to having either apprentice-type employees that come with unique challenges or pulling from an aging workforce that can bring cumulative injuries and risks. Navigating these issues can be complex and there is not a perfect solution, but employer’s hiring practices need to change in order to keep up with the current state of the industry.

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

With unemployment rates settling near 4%, it is becoming increasingly difficult to find the right employees to help grow your construction company. With most able-bodied workers having secure employment, this leads to having either apprentice-type employees that come with unique challenges or pulling from an aging workforce that can bring cumulative injuries and risks. Navigating these issues can be complex and there is not a perfect solution, but employer’s hiring practices need to change in order to keep up with the current state of the industry.

When hiring new employees, consider:

Pre-hire drug testing

Pre-hire physicals

Targeted job postings with accurate description of daily work

Multiple levels of interviews

Simulating work at your office that potential new hires would be performing in the field

The US saw a unique shift in the workplace as a result of COVID-19 where employees felt their value skyrocket as fewer people were willing to work in-person. Employers were forced to increase wages to get bodies on jobsites. In prior years, it may have been enough to just rely on word of mouth and referrals to get new hires. Too often now, we are seeing new hires suffer “ghost injuries” that are quickly followed with letters of representation. These and similar types of cumulative trauma claims can have long term impacts on your experience rating (EMR). While these situations are difficult to prevent, using best practices and conducting thorough interviews with your prospective employees will allow you to make educated decisions which typically lead to better hires.

Taking advantage of the best practices listed above can help insulate your company from poor hiring decisions. Obviously, we would love for new hires to turn into long term employees, as onboarding and proper training can be a costly expense in both other employee’s time and payroll. In a recent survey conducted by Traveler’s Insurance, it was shown that 34% of workplace injuries occurred during the worker’s first year on the job. This can be from a combination of inexperience, overexertion, and/or lack of safety knowledge.

Consider these hiring and onboarding processes to assist in mitigating the glaring number of claims that are emanating from newer employees or employees that have limited experience on jobsites. The financial impact they can have on your company will impact your balance sheet for years and can be potentially avoided with implementing some of our recommended techniques

To learn more about improving your hiring practices or how Rancho Mesa can help to improve your process, reach out at (619) 438-6900 or ccraig@ranchomesa.com.

Properly Utilizing Tailgate Meetings

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

For many foremen and superintendents, weekly tailgate meetings can feel like a task that just needs to be checked off the list. However, while the purpose of these meetings is critical for the health and well-being of fellow field employees, the time required and repetitive nature of them can create challenges. To maximize the benefits of these meetings, construction firms must be proactive and thoughtful as they develop an inventory of topics.

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

For many foremen and superintendents, weekly tailgate meetings can feel like a task that just needs to be checked off the list. However, while the purpose of these meetings is critical for the health and well-being of fellow field employees, the time required and repetitive nature of them can create challenges. To maximize the benefits of these meetings, construction firms must be proactive and thoughtful as they develop an inventory of topics.

Identifying Tailgate Meeting Topics

Take ample time with your sales team to understand the scope of your backlog to see where hazards may appear within these projects. Plan training topics with an eye on the weather, paying close attention to historically warm or cold months. Consider connecting with your insurance broker as well on recent injury trends that you can address with the crew.

This will be pertinent as your company approaches their renewal window with underwriters looking at claims history. They commonly ask, “what has the insured done to make sure these claims don’t happen again?” Learning from your past is key to being proactive. Knowing you will have certain exposures coming up and addressing those with preventative training topics begins to build a Best Practice Safety Program.

Accessing Content for Training

Locating “Toolbox” trainings can be time consuming and, in some cases, costly. And very often, the trainings may not be applicable to your operation and/or the trends you may need to focus on. With an eye to the future, Rancho Mesa has recently introduced a proprietary SafetyOne™ App. Safety managers will be able to document safety inspections from their mobile device and assign required fixes to employees, while also tracking when they have been completed. Meeting content can also be distributed to supervisors through their mobile device all with a focus of making safety meetings more efficient and effective. These same supervisors can now access a vast library that can be customized to their operation.

Reach out to me to learn more about the SafetyOne™ App and how Rancho Mesa can partner with you and your team moving forward. You can reach me at (619) 438-6900 or email me at ccraig@ranchomesa.com

Construction Death Rate Not Decreasing as Expected

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

With the heightened safety regulations and OSHA guidelines over the past decade, many would think we are working in a much safer environment with fewer fatalities. Despite the rising number of employees and using a standard based off deaths per 100,000 employees, the data is showing that the number of fatalities are the same as they were a decade ago.

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

With the heightened safety regulations and OSHA guidelines over the past decade, many would think we are working in a much safer environment with fewer fatalities. Despite the rising number of employees and using a standard based off deaths per 100,000 employees, the data is showing that the number of fatalities are the same as they were a decade ago.

With a much larger workforce, OSHA is severely understaffed compared to the previous decade. The agency does not have enough inspectors to visit nearly enough jobsites. They have been more reactive in the sense that they are imposing fines on companies after they have had losses. These fines represent a fraction of what it would take to motivate construction companies to revamp their respective safety programs. Employers have factored these fines into the cost of business to a certain extent.

OSHA is now contemplating whether it is worth doubling the jobsite inspections annually and/or increase fines drastically. There is no solid data to link an increase in jobsite inspections to fewer fatalities, so the logical answer would be heavier fines and a push for more negligent death claims to be criminally prosecuted.

Either of these options will lead to more oversite or more fines for the construction industry as a whole. One critical approach you can take is to prepare yourself as a business owner. Be proactive. Consider working with the consultation branch of OSHA to visit your operation and jobsites. This division within OSHA does not issue fines or violations. They do, however, offer recommendations and advice on how to make your operation safer. With the potential of OSHA’s fines increasing, it is time to make sure that your company is on the forefront of safety. A great first step is reaching out to your insurance broker to help you meet requirements and push you to exceed. With a potential recession looming, it is important to make sure you have insulated your company from risk, so you have the best chance at thriving.

If you have any urgent questions on this topic, you can reach me directly at (619) 438-6900 or email me at ccraig@ranchomesa.com.

The Link Between Your EMR and Primary Threshold

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

One of the biggest concerns for contractors is their Experience Modification Rating (EMR). If your EMR exceeds 1.00 or 1.25, contractors can be removed from bid lists and premiums can escalate quickly. Most decision makers have little idea what factors contribute to the EMR and just how claims can impact them.

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

One of the biggest concerns for contractors is their Experience Modification Rating (EMR). If your EMR exceeds 1.00 or 1.25, contractors can be removed from bid lists and premiums can escalate quickly. Most decision makers have little idea what factors contribute to the EMR and just how claims can impact them.

All construction companies are assigned class codes that best define their operations and those class codes have expected loss rates associated with them. The more losses that occur per $100 of payroll for that class code, the larger the expected loss rate will be. So, an electrician with a much lower expected loss rate than a roofing contractor will have each claim impact their EMR more. These are variables that can have a significant impact on your company’s EMR. The variable that fluctuates amongst each company is the amount of payroll they develop in each class code. The more payroll generated, the lower your best possible EMR can be.

Consequently, as a company’s best possible EMR decreases, the Primary Threshold increases. The Primary Threshold is a cap or threshold unique to each company. The higher the primary threshold, the less that any one claim can impact your EMR. For example, a painting contractor using the 5474 class code and averaging $200,000 a year in payroll will have a best possible EMR of 83 and primary threshold of only $8,500. Each claim has the potential of contributing 40 points to their EMR. While another painter that averages $10,000,000 in payroll will have a best possible EMR of 41 and primary threshold of $49,000. Thus, the maximum any one claim can impact the company with higher payroll is just 5 points.

This certainly is a drastic difference but it makes sense as the larger company has more employees which leads to more exposure and more expected losses. The component that most companies do not know well enough is that for each company in the examples above, the WCIRB penalizes the exact same for any claim that exceeds your primary threshold. So, for the smaller company, an $8,500 claim is worth 40 points to their EMR, a $1,000,000 claim is worth the exact same amount. And, the same for the larger company with a $49,000 claim worth 5 points but any claim dollars in excess of that will not impact the EMR.

Taking this information into account, we urge our clients to focus on mitigating claims before they happen as well as doing their best to reduce contributing factors such as temporary disability. Having your carrier pay for your employees missed time leads to your EMR increasing and your premiums inevitably being higher than you would like.

Understanding and implementing a return-to-work program is extremely beneficial to your company and leads to you saving money over time. Working with your broker to better understand how to properly handle claims and making sure you are doing everything possible to keep your EMR as low as possible is vital to your company’s profitability and is very much in your control.

Everyone wants a better EMR and lower premiums but the elite contractors are active in not only preventing claims from happening but understanding how important it is to keep their employees at the workplace, or at the very least, off the couch at home.

If you would like to learn more about your firm’s primary threshold or how it is impacting your company, please do not hesitate to reach out to me directly at ccraig@ranchomesa.com or call me at (619) 438-6900.

Wage Inflation’s Impact On Workers’ Compensation

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

Following up on a great article by fellow construction team member Kevin Howard, about anticipated wage threshold increases coming in 2022, I wanted to highlight the building problems resulting from substantial hourly wage increases.

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

Following up on a great article by fellow construction team member Kevin Howard, about anticipated wage threshold increases coming in 2022, I wanted to highlight the building problems resulting from substantial hourly wage increases.

I specialize in painting, drywall and plastering contractors and have been asking my clients over the past few months about the health of their business and any new challenges. The most common answer: there is a substantial amount of work to bid on, but a labor shortage limits the possibility of growth.

Paying an employee higher wages creates new issues. Employees tend to inform co-workers when they get a raise. Employees may also try to leverage another company’s higher wage into a raise. The combination of a labor shortage and overpaying employees may result in hyperinflation, leading these employees to believe their value has skyrocketed.

Tying back into Kevin’s article, it is easy to see why these thresholds need to be increased. The wage threshold is meant to separate historically safer employees from newer employees who are less safety conscious. These increases in payroll are pushing less skilled employees into the higher wage category, resulting very likely in higher claim frequency as they are historically less experienced and safety conscious on the jobsite. This is leading to a smaller gap in workers’ compensation rates between the above and below class codes for each industry.

For example, a painter had a separation of 56% from 5474 to 5482 (painters making above or below $28) for their 2021 renewal. For 2022, they are only looking at a 46% difference. From the carrier perspective, more losses are expected in the 5482 (above $28) than the previous year, leading to a rate increase in that class code. I wish I could say that this was industry specific, but from conversations with multiple underwriters, most industries are dealing with these same employment issues and have struggled to find meaningful solutions.

It is possible these dual wage threshold increases will help restore balance by bringing the less skilled employees back into the proper class code, securing the lower rates in the over class code. Employers have shared that these threshold increases are hurting them, but should assist with workers’ comp savings for the truly elite seasoned workers. Carriers have these thresholds to help you differentiate experience from inexperience.

This is a developing issue that we are trying to stay ahead of. The time is now to meet with someone who specializes in your industry and help you formulate a strategy for 2022 to mitigate these impacts and improve your profitably. To schedule a time to talk or meet with me or you can call me directly at 619-438-6900.

Timely Reporting of Workers’ Compensation Claims Lower Overall Costs

Author, Jack Marrs, Associate Account Executive, Rancho Mesa Insurance Services, Inc.

Leading into 2022, it is important for employers to examine their workplace injury reporting practices. Specifically, employers should report all injuries including medical-only workplace injuries to their workers’ compensation insurance company. Best practices dictate all claims should be reported within the first 24 hours in order to improve treatment to the injured worker and reduce the overall cost of the claim to the employer.

Author, Jack Marrs, Associate Account Executive, Rancho Mesa Insurance Services, Inc.

Leading into 2022, it is important for employers to examine their workplace injury reporting practices. Specifically, employers should report all injuries including medical-only workplace injuries to their workers’ compensation insurance company. Best practices dictate all claims should be reported within the first 24 hours in order to improve treatment to the injured worker and reduce the overall cost of the claim to the employer.

A recent conversation with an underwriting manager highlighted the fact that some employers are choosing to pay for occupational clinic visits rather than filing a claim, assuming that small medical-only claims will negatively impact the Experience Modification Factor (X-mod) and ensuing workers’ compensation premiums. However, in actuality claims of $250 or less do not impact the X-mod. Not only are employers legally required to report workplace injuries, but those small claims can easily turn into something bigger, if not reported in a timely manner. Further, the reporting of all incidences can assist a company in identifying trends and root causes thereby allowing for proactive measure to be taken. Rancho Mesa’s proprietary Key Performance Indicator (KPI) dashboard helps track these trends and compare a company’s performance to that of their industry. Request a KPI dashboard for your company.

Why then does reporting lag result in higher claim costs? An insurance carrier’s ability to investigate a claim, determine compensability, and identify fraud may be hindered as details of the incident fade, witnesses may no longer be available or key evidence may not be preserved. According to Liberty Mutual, a 29-day delay in reporting an injury can lead to a 33% increase in lost time, 52% higher average claim cost, and 152% increase in litigation rates. This makes sense when one considers that a delay in seeking treatment could cause an employee’s condition to worsen, extending recovery time and temporary disability payments.

Lastly, an employer paying a medical bill will pay much more than a workers’ compensation carrier would pay for that same bill as insurance companies negotiate a reduced fee schedule for occupational injuries. Bottom line, failure to report workplace incidents in a timely manner can put any organization and its employees at risk for no benefit. Contact Rancho Mesa to learn more about our Risk Management Center and how our free trainings and webinars can improve your reporting practices.

2022 Construction Dual Wage Thresholds - An Early Look

Author, Kevin Howard, Account Executive, Rancho Mesa Insurance Services, Inc.

There are 16 construction workers’ compensation class code pairs in California, each set up as dual wage classifications. The purpose of these “split” class codes allows the Workers’ Compensation Insurance Rating Bureau (WCIRB) and California insurers to better predict future risk and underwrite with more accuracy.

Author, Kevin Howard, Account Executive, Rancho Mesa Insurance Services, Inc.

There are 16 construction workers’ compensation class code pairs in California, each set up as dual wage classifications. The purpose of these “split” class codes allows the Workers’ Compensation Insurance Rating Bureau (WCIRB) and California insurers to better predict future risk and underwrite with more accuracy.

To illustrate the dual wage threshold, consider a seasoned laborer with years of safety training, exposure awareness, and familiarity with jobsite protocol. This employee is going to be less of a safety risk compared to an apprentice who is still learning his or her trade, the safety techniques and all of the skill associated with a trade. As one might imagine, statistics consistently show a much higher probability of an injury occurring with an apprentice versus a seasoned veteran or journeymen. So, having a dual wage threshold allows carriers to generate pricing based on the employees’ experience and likelihood of having an injury.

Exploring how this can directly impact rates and pricing, the 2021 roofing dual wage class codes of 5552 and 5553 is a great example.

Class code 5552 is defined as roofers who make less than $27 per hour. The average California worker’s compensation insurance base rate for this class code is $40 per $100 of payroll. Class code 5553 includes roofers who make $27 or more per hour. This class code’s average California workers’ compensation insurance base rate is $20 per $100 of payroll. In this example, the workers’ compensation premium base rate is half the cost for a more experienced employee over someone with less experience.

It is crucial for any roofing contractor to be mindful of this wage threshold data knowing that the delta in the 2022 recommended increase represents a staggering 61% gap between the two base rates.

Additionally, the WCIRB has continued to increase wage thresholds. This is to keep up with inflation of the US dollar, the increase in minimum wage and the demand for labor, among other factors.

Dual Wage Classification Thresholds by Year

Shown below are the wage thresholds for all dual wage classifications. For information about these classifications, see the California Workers' Compensation Uniform Statistical Reporting Plan—1995, effective September 1, 2021.

| Classifications | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Year | 5027 | 5140 | 5183 | 5185 | 5201 | 5403 | 5446 | 5467 | 5474 | 5484 | 5538 | 5552 | 5632 | 6218 | 6307 | 6315 |

| 5028 | 5190 | 5187 | 5186 | 5205 | 5432 | 5547 | 5470 | 5482 | 5485 | 5542 | 5553 | 5633 | 6620 | 6308 | 6316 | |

| 9/1/2022 | $32 | $34 | $31 | $32 | $32 | $39 | $38 | $36 | $31 | $36 | $29 | $29 | $39 | $39 | $39 | $39 |

| 9/1/2021 | $28 | $32 | $28 | $29 | $28 | $35 | $36 | $33 | $28 | $32 | $27 | $27 | $35 | $34 | $34 | $34 |

| 1/1/2021 | $28 | $32 | $28 | $29 | $28 | $35 | $36 | $33 | $28 | $32 | $27 | $27 | $35 | $34 | $34 | $34 |

| 1/1/2020 | $28 | $32 | $28 | $29 | $28 | $35 | $36 | $33 | $28 | $32 | $27 | $27 | $35 | $34 | $34 | $34 |

| 1/1/2019 | $27 | $32 | $26 | $27 | $25 | $32 | $34 | $32 | $26 | $29 | $27 | $25 | $32 | $31 | $31 | $31 |

| 1/1/2018 | $27 | $32 | $26 | $27 | $25 | $32 | $34 | $31 | $26 | $29 | $27 | $25 | $32 | $31 | $31 | $31 |

| 1/1/2017 | $27 | $30 | $26 | $27 | $24 | $30 | $33 | $31 | $24 | $27 | $27 | $23 | $30 | $30 | $30 | $30 |

© 2021 Workers' Compensation Insurance Rating Bureau of California. All Rights Reserved.

WCIRB’s 2022 RECOMMENDATION:

The Bureau is considering raising the hourly wage threshold for all 16 dual wage classification pairs with some codes seeing as much as a $5.00 increase. The average delta between the lower advisory rate and higher advisory rate is 48%.

Proposed Dual Wage Threshold Increases

| Dual Wage Classifications | Existing Threshold | Proposed Increase | Proposed Threshold | Low Wage Advisory Rate | High Wage Advisory Rate | % Difference From Low Wage Rate |

| 5027/5028 Masonry | $28 | $4 | $32 | $8.18 | $4.21 | -48.50% |

| 5190/5140 Electrical Wiring | $32 | $2 | $34 | $3.76 | $1.45 | -61.40% |

| 5183/5187 Plumbing | $28 | $3 | $31 | $5.31 | $2.36 | -55.60% |

| 5185/5186 Automatic Sprinkler | $29 | $3 | $32 | $4.57 | $1.00 | -57.30% |

| 5201/5205 Concrete Work | $28 | $4 | $32 | $6.64 | $1.95 | -36.30% |

| 5403/5432 Carpentry | $35 | $4 | $39 | $10.03 | $4.23 | -55.10% |

| 5446/5447 Wallboard Installation | $36 | $2 | $38 | $5.42 | $4.50 | -55.10% |

| 5467/5470 Glaziers | $33 | $3 | $36 | $7.62 | $2.65 | -59.30% |

| 5474/5482 Painting Waterproofing | $28 | $3 | $31 | $8.09 | $3.10 | -46.40% |

| 5484/5485 Plastering or Stucco | $32 | $4 | $36 | $9.98 | $4.34 | -37.40% |

| 5538/5542 Sheet Metal Work | $27 | $2 | $29 | $5.07 | $2.52 | -50.30% |

| 5552/5553 Roofing | $27 | $2 | $29 | $21.05 | $8.14 | -61.30% |

| 5632/5633 Steel Framing | $35 | $4 | $39 | $10.03 | $4.50 | -55.10% |

| 6218/6220 Grading/Land Leveling | $34 | $5 | $39 | $5.10 | $2.93 | -42.50% |

| 6307/6308 Sewer Construction | $34 | $5 | $39 | $6.98 | $2.84 | -59.30% |

| 6315/6316 Water/Gas Mains | $34 | $5 | $39 | $4.18 | $3.70 | -11.50% |

This recommendation, if approved by the insurance commissioner, would become effective September 1, 2022.

With the continuing labor shortage in the construction arena, employers have been doing everything possible to retain employees by offering richer benefits plans, pay increases and merit bonuses, when applicable. These recommended wage classification increases could potentially push employers to extend additional pay raises to employees in an effort to minimize workers’ compensation premiums.

It is best for contractors who utilize any of the 16 dual wage classification pairs to be aware of the potential increases and to do the math to see if it makes sense to consider raises prior to your 2022-2023 September 1st workers’ compensation renewal.

Rancho Mesa predicts that this info will become a major factor in payroll decisions based on overhead cost management and recommend this as a topic for discussion early so that our clients, prospects and listeners can prepare.

To discuss how the proposed dual wage threshold increases may affect your business, contact me at (619) 438-6874 or khoward@ranchomesa.com.

Top Five Workers’ Compensation Claims That Impact a MEP’s Bottom Line

Author, Amber Webb, Account Executive, Rancho Mesa Insurance Services, Inc.

If you are an MEP contractor who wants to impact both your productivity and profitably, then the following is crucial for your success. Our MEP Group at Rancho Mesa understands the importance of identifying the top five workers’ compensation claims that impact your industry while providing pertinent resources to help mitigate that risk.

Author, Amber Webb, Account Executive, Rancho Mesa Insurance Services, Inc.

If you are a Mechanical, Electrical & Plumbing (MEP) contractor who wants to impact both your productivity and profitably, then the following is crucial for your success. Our MEP Group at Rancho Mesa understands the importance of identifying the top five workers’ compensation claims that impact your industry while providing pertinent resources to help mitigate that risk. By working with leading workers’ compensation carriers and the Occupational Safety and Health Administration (OSHA), we identified the top 5 workers’ compensation claims affecting the MEP industry:

Cut/Puncture/Scrape/Lacerations

Slip/Falls from both same level and ladders/scaffolding

Strains from lifting/handling/pushing/pulling

Struck by object/Foreign Body in Eye

Motor Vehicle Accident (injured employee)

With employee safety at the forefront of your operations, understanding where the claims are likely to come from and then having the support and tools in place to address those concerns is vital to your long term success. When injuries occur on the job, it impacts not only the life of the injured worker and their family but will directly impact the productivity and profitability of the project.

For our clients to proactively mitigate these exposures, we provide them with access to specific trainings related to these top MEP claims and OSHA citations from our Risk Management Center Library. Our Client Services team then works closely with our clients to customize their trainings while meeting their specific risk management needs.

If you are not already a Rancho Mesa client, and would like a free trial of our Risk Management Center, please complete the form or contact Amber Webb at (619) 486-6562 or awebb@ranchomesa.com.

California’s Landscape Industry Prepares for Ex-Mod Changes

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

For the first time in several years the Expected Loss Rate for class code 0042 has increased from $2.38 to $2.42, a 2% increase.

Bottom line, although very minimal, this should help bring the experience mod down.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

For the first time in several years the Expected Loss Rate for class code 0042 has increased from $2.38 to $2.42, a 2% increase.

Bottom line, although very minimal, this should help bring the experience mod down.

This information will impact any landscape company who has a policy effective date of September 1, 2021 and beyond.

Based on a couple of projection comparisons, we have seen an impact of 1 to 4 points come off the experience mod for landscape companies.

Landscape companies working with Rancho Mesa with policy effective dates after 9/1/2021 will see updated information on their KPI Dashboard, at the next review.

For landscape companies not working with Rancho Mesa, you can request a custom KPI Dashboard today by reaching out to Drew Garcia.

Profitable Bids Should Include Often Overlooked Insurance Costs

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

We will take a look at factors that go into your bid and ways to ensure you are hitting your target profit margin. There are many factors that go into creating a profitable bid on a construction project. They include…

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

We will take a look at factors that go into your bid and ways to ensure you are hitting your target profit margin.

There are many factors that go into creating a profitable bid on a construction project. They include:

The scope of the work

The location of the project

Material costs

Labor costs

For most construction companies, their estimators are well versed in all of the areas mentioned earlier and yet despite their best efforts, an unforeseen circumstance may occur and drive up the cost of a project, resulting in reduced profitability or a loss on the project.

One area that is often overlooked, but controllable, is the impact insurance has on the profitability of the project. The question to ask is how prepared are you and your staff to address the following questions:

Do you have the required insurance, coverages, limits, and terms in place to meet the contractual requirements of the project? If not, what will be the cost to add those requirements?

Will the project overlap your insurance renewal? If so, what changes in your Experience Modification Rate (EMR) can you anticipate and what will be the dollar impact?

What changes in your General Liability and Excess Insurance rates can you expect?

Working with your insurance advisor on the above is a necessary step is helping to create a better opportunity for profitable jobs. At Rancho Mesa, we follow strict Best Practices and have prescheduled meetings with our insureds throughout the policy term, but additionally conduct a focused pre-renewal meeting 120 days prior to policy expiration.

Those meetings allow us to:

Keep our clients aware of changes in the insurance marketplace that may impact their business.

Project their EMR for the coming year and discuss how this might influence your bidding process.

Review industry workers’ compensation trends in both Pure Premium Rates and Expected Loss Rates and their impact on workers compensation costs.

So, work with your insurance advisor and uncover those overlooked insurance costs to minimize risk and maximize profitability. To understand these factors in more detail or to look at our new KPI Dashboard that puts this information at your fingertips you can reach me at 619-486-6900 or ccraig@ranchomesa.com.

New Hires Pose Hidden Exposure

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

Hiring is never an easy task, especially during a pandemic. Dealing with COVID-19 has made finding the right employees much more difficult for many business owners in the construction industry. Now is the perfect time to evaluate your hiring practices to ensure you don’t make a costly hiring mistakes that can affect your Experience Modification Rate (XMOD) and workers’ compensation premium long after the pandemic has passed.

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

Hiring is never an easy task, especially during a pandemic. Dealing with COVID-19 has made finding the right employees much more difficult for many business owners in the construction industry. Now is the perfect time to evaluate your hiring practices to ensure you don’t make a costly hiring mistakes that can affect your Experience Modification Rate (XMOD) and workers’ compensation premium long after the pandemic has passed.

It was not that long ago that our economy was thriving and we had an unemployment rate under 4% in California. Though, due to the shutdown, we have seen that number shoot up as high as 16.4% in April 2020 and settle back down to 11% by September 2020, according to the Bureau of Labor Statistics (BLS). So, while many industries saw massive lay-offs, the construction industry has continued to thrive, at least for the time being. That means many employers are now actively looking for both skilled and non-skilled labor in order to complete existing projects and plan for future contracts that have been awarded. That’s great news for the 11% of the population who are unemployed, but employers should still be cautious about hiring just anyone without utilizing best practices to minimize risk.

In September 2020, Rancho Mesa partnered with Culture Works to offer the “Remote Recruiting & Company Culture Webinar” where they went into detail on the best practices for remote recruiting. Watch an archived version of the webinar to learn practical steps for recruiting employees in today’s economic climate.

Finding the right employee for the job may not be as easy as it used to be. Some skilled workers may not feel comfortable working on a job site, even while safety precautions are being observed. And, others may have been offered higher wages and more benefits at other companies who are also in need of workers. So, employers are really at a disadvantage. They may weigh the benefits and risks of hiring people who are less experienced or those who don’t take job site safety very seriously.

Now is the time to implement best practices when hiring to insulate your company from potential problems. This could mean implementing drug testing, pre-hire physicals, reach out to previous employers for recommendations, and updating your employee handbook to making sure these employees are aware of exactly what the job description is that they are being hired to do and the company’s expectations.

Experience on the job and a history of safety training are indicators that a new hire is a good risk. However, we know that employees over 45 have a 23% higher chance of having a sprain, strain or tear than employees under the age of 45. They also have a 27% higher chance of having a slip, trip or fall according to BLS. This does not mean that you shouldn’t hire workers over 45. It just means that to minimize risk, provide employees with appropriate training. Implement stretch and mobility programs for your workforce to do daily to reduce the exposure.

Rancho Mesa offers clients the Field Mobility & Stretch and ABLE Lifting training that is designed to reduce strains and cumulative trauma claims. Getting your employees prepared for the work day before they pick up their tools is vital in staying ahead of claims and boosts employee morale. The best way to handle workers’ compensation claims is to prevent them from happening.

Knowing your exposure is vital in staying ahead of industry trends. If you have further questions do not hesitate to contact me at (619) 438-6900 or ccraig@ranchomesa.com.

Work Comp Unit Stat: The Meeting That Saves You Money

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

California business owners are aware that their experience modifier (XMOD) is published annually, roughly three to four months before the expiration of their current workers compensation policy term. However, more often than not, companies are missing an incredible opportunity to make an impact on the calculation of their XMOD by strategically evaluating their work comp claims prior to the most critical month in the XMOD calendar known as Unit Stat.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

California business owners are aware that their experience modifier (XMOD) is published annually, roughly three to four months before the expiration of their current workers compensation policy term. However, more often than not, companies are missing an incredible opportunity to make an impact on the calculation of their XMOD by strategically evaluating their work comp claims prior to the most critical month in the XMOD calendar known as Unit Stat.

The Workers’ Compensation Insurance Rating Bureau (WCIRB) defines the process of receiving loss and payroll information by classification as the Unit Statistical Report. The information is reported to the WCIRB by insurance carriers at specific intervals based on your company’s policy effective date. The information is valued for the first time 18 months after the inception of your policy and every 12 months thereafter.

A policy that incepts in January 2020 will be valued for the first time in July of 2021 (18 month mark). This information will remain in your XMOD calculation for the valuations at 30 months and 42 months.

Once this information has been received by the WCIRB, from the respective carriers, it cannot be altered or changed until the following year’s unit stat. Thus, you may have a positive outcome on an existing open claim (reserve reduction or closure) but not see the benefit until the following year. Revisions to the XMOD once published are limited to a few circumstances; more information about revisions can be found here.

The loss information, sent to the WCIRB from the insurance carriers, will be evaluated at the paid (closed claim) or reserved (open claim) amounts. Typically, a claim that has been open for longer than 18 months signifies severity, litigation, lost time, permanent disability, or a combination of the group. For this reason it is absolutely critical that as a part of your risk management process you execute a

pre-unit stat meeting.

When should I schedule my Unit Stat meeting?

What should I do at this meeting?

Who needs to be involved?

How will this meeting save me money?

As a client of Rancho Mesa, we build this meeting into your annual service plan and take care of engaging the parties who need to be involved for the betterment of your XMOD.

Ready to learn more about Unit Stat? Join us for a complimentary 25-minute webinar where we will discuss the process in greater detail and take time for Q&A.

Still not sure if further learning is necessary, ask yourself these questions:

Have you ever been surprised by your XMOD being higher than you would have thought?

Have you ever had an XMOD above 1.00?

Has your XMOD ever caused your premium to increase?

The webinar can be viewed on-demand by clicking the link below.

2019 Expected Loss Rates Published in California’s Updated Regulatory Filing – X-MOD Impact Inevitable for 0042 Class Code

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

The 2019 Expected Loss Rate (ELR) for Landscaping class code 0042 was recently published at a 15% decrease or $2.97.

The ELR is the factor used to anticipate a class code’s claim cost per $100 for the experience rating period. It is not to be confused with the Pure Premium Rate (PPR). The ELR differs from the PPR in that the ELR simply measures the basic claim cost for a class code without including loss adjustment expense, excess loss load (capped at $175,000 for X-MOD purposes), and loss development.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

The 2019 Expected Loss Rate (ELR) for Landscaping class code 0042 was recently published at a 15% decrease or $2.97.

The ELR is the factor used to anticipate a class code’s claim cost per $100 for the experience rating period. It is not to be confused with the Pure Premium Rate (PPR). The ELR differs from the PPR in that the ELR simply measures the basic claim cost for a class code without including loss adjustment expense, excess loss load (capped at $175,000 for X-MOD purposes), and loss development. The PPR includes all of the mentioned above factors and is the rate for which a carrier can expect to pay for all of the cost associated with claims in a specific industry. The PPR does not account for the carrier’s overhead, profit, tax, and commissions.

Under most circumstances, when you hear the word decrease as associated with insurance its a good thing, but in the case of the ELR, a decrease will have a negative impact on your Experience MOD (X-MOD). In simple terms, if your losses stay the same and the ELR for your industry is down 15%, your X-MOD is going to go up.

At 15%, the landscape class code accounts for one of the largest swings in the 2019 regulatory filing for all industries. This only reinforces the importance of mitigating claim frequency, superior carrier claims handling, internal claims advocacy, claim cost consolidation efforts, and a proven system to keep all of these aspects running constantly. Fortunately, Rancho Mesa has a system in place today and it is a proven success.

Don’t be caught off guard in 2019; have a plan and always anticipate for the future. Let Rancho Mesa help manage your landscape insurance needs. For more information, call (619) 937-0164.

Distracted Driving, Not Just an Automobile Insurance Issue, Bad News for Workers Compensation Too

Author, David J Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

I’ve written at length on the negative effects distracted driving is having on the automobile insurance industry and its impact on the rise in accidents, claim costs, and increases to your automobile premiums. But, have you considered its effects on your Experience Modification Rate (EMR) and ultimately workers’ compensation cost?

Author, David J Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

I’ve written at length on the negative effects distracted driving is having on the automobile insurance industry and its impact on the rise in accidents, claim costs, and increases to your automobile premiums. But, have you considered its effects on your Experience Modification Rate (EMR) and ultimately workers’ compensation cost?

When one of your employees is injured in an automobile accident while working on your behalf, Arising out of Employment (AOE) / Course of Employment(COE) their sustained injury will be covered by your workers’ compensation policy, regardless of fault.

“Regardless of fault?!”

When a third party is deemed at fault and the injuries to your employee(s) have been settled, your workers’ compensation insurance carrier may “subrogate” their costs to the carrier representing the at fault driver. Now, here is the realty – studies have shown that 14.7% (4.1 million) of all California drivers are uninsured, while another large percentage of drivers hold the California minimum limits of $15,000/$30,000. What this means is that even if subrogation is a possibility, the likelihood of a “full” recovery is not probable. Thus, all the costs of the injury to your employee(s) will likely be the sole responsibility of your workers’ compensation carrier and this claim cost negatively affects your EMR and loss ratios for years to come.

What can you do?

You can implement a strong fleet safety program that includes a policy pertaining to distracted driving. When your employee is involved in a motor vehicle accident, adherence to your company’s accident investigation protocol is crucial. Documentation will prove pivotal for your carrier if subrogation becomes a possibility.

For our clients, through RM365 Advantage, we have a number of resources: fleet safety programs that can be customized, fleet safety training topics, fillable and printable accident investigation forms, archived fleet safety workshop videos, and more, in both English and Spanish. You can access this through our RM365 Advantage Risk Management Center or contact our Client Services Coordinator Alyssa Burley at aburley@ranchomesa.com.

If you are not a current client of Rancho Mesa, we encourage you to reach out to your broker for assistance or email Alyssa Burley to get additional information or to ask any questions.

Changes in the 2019 Experience Modification Formula – Are You Ready? (Part 2)

Author, David J. Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

As we approach 2019, there will be several changes in the experience modification formula that directly affects the calculation of an employer's 2019 Experience Modification Rate (EMR).

Part 1 of this article describes the Primary Threshold and Expected Loss Rate. Read Part 1 of this article. Part 2 provides an overview of the changes to the EMR calculation.

Author, David J. Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

As we approach 2019, there will be several changes in the experience modification formula that directly affects the calculation of an employer's 2019 Experience Modification Rate (EMR).

Part 1 of this article describes the Primary Threshold and Expected Loss Rate. Read Part 1 of this article. Part 2 provides an overview of the changes to the EMR calculation.

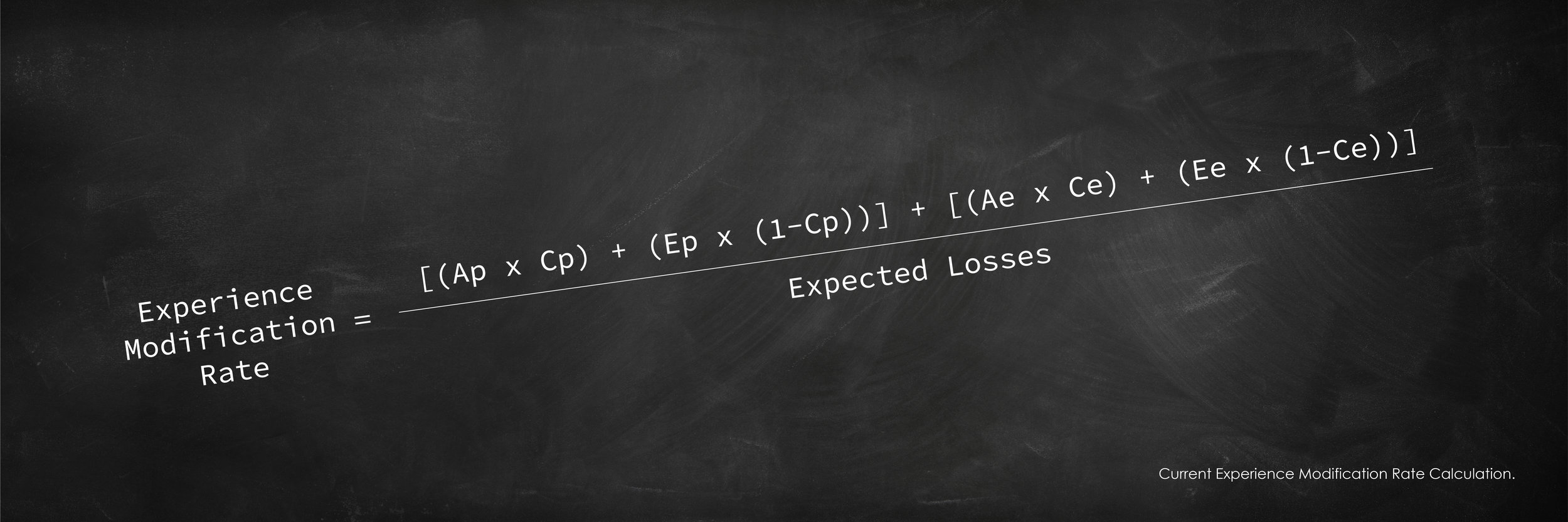

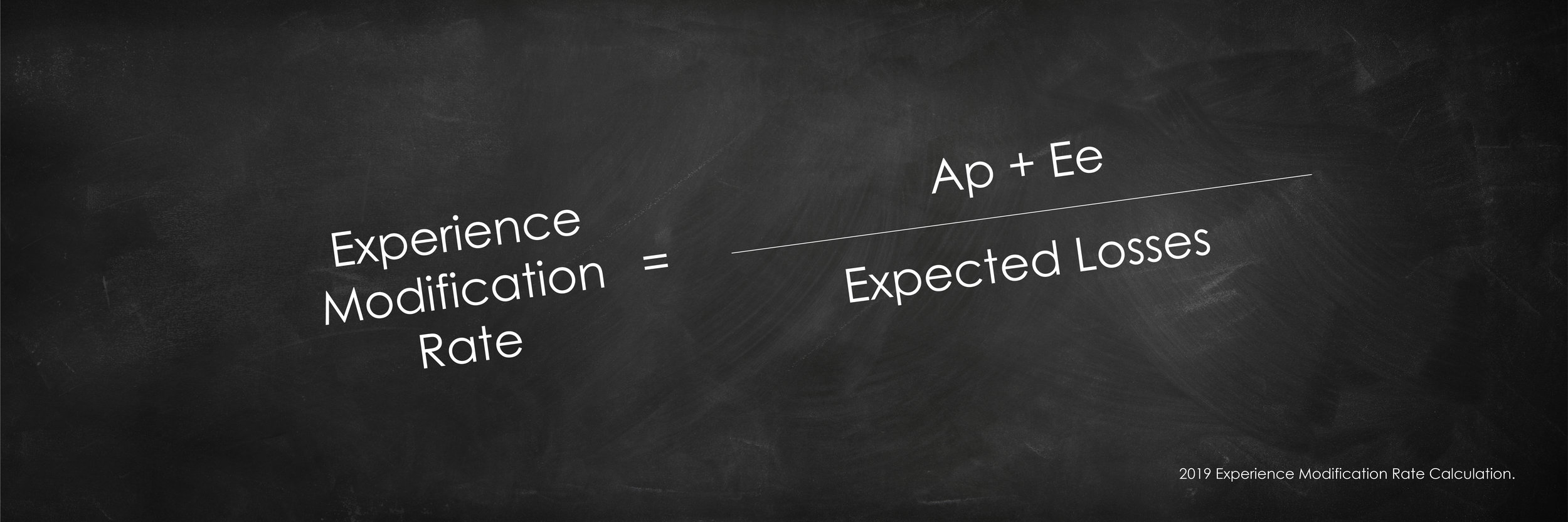

The Simplified Formula

Individual claim cost (i.e., both paid and reserved) will go into the calculation up to the primary threshold limit are considered the actual primary losses. Any claim cost that exceeds your primary threshold is considered the actual excess loss. In past experience mod formulas, the actual excess loss was used in the factoring of your EMR; in 2019, it will have no effect. However, under the new calculation, the industry expected excess losses will be considered in the 2019 simplified formula.

Actual Primary Losses + Expected Excess Losses / Expected Losses

The expected excess losses are calculated by multiplying your class code’s payroll per $100 by the expected loss rate for that same class code. This number is then discounted by the “D Ratio” to determine expected primary losses and expected excess losses. There are 90 different D-Ratios for each classification based on the primary threshold. The D-Ratio is different for each classification and is determined by the severity of injuries that occur within that particular class code.

The first $250 of all claims will no longer be used in the calculation of your EMR.

This is a major change and one that was initiated in part to encourage all employers to report all claims, including those deemed first aid, without having a negative impact on the companys’ EMR. This change will affect all claims within the 2019 calculation; so yes, it will include years previously completed and reported. This will have a positive impact on EMRs in that claim dollars will be removed from the EMR calculation.

Confused – Want more details?

Help is on the way. We are going to hold a statewide webinar on Thursday, October 4th at 9:00am in order to dig deeper into this subject and answer specific questions. You may register for the webinar by contacting Alyssa Burley at (619) 438-6869 or aburley@ranchomesa.com.

Changes in the 2019 Experience Modification Formula – Are You Ready? (Part 1)

Author, David J. Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

As we approach 2019, there will be several changes in the experience modification formula that directly affects the calculation of an employer's 2019 Experience Modification Rate (EMR). Sadly, most businesses are both unaware and unprepared.

Author, David J. Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

As we approach 2019, there will be several changes in the experience modification formula that directly affects the calculation of an employer's 2019 Experience Modification Rate (EMR). Sadly, most businesses are both unaware and unprepared.

Before we breakdown the changes to the 2019 EMR formula, we must first have a strong understanding of the two critical components that directly affect the outcome of the EMR. This article will be broken out into 2 parts. Part 1 will describe the Primary Threshold and Expected Loss Rate. In Part 2, I will provide an overview of the changes to the EMR calculation.

The single most important number to my EMR is not my final rating?

Primary Threshold

Rancho Mesa has long taken a stance on the importance of a business owner knowing their primary threshold as it relates to the EMR. Proactive business owners should monitor their primary threshold annually as it is subject to change due to payroll fluctuations, operations, and the annual regulatory filing of the expected loss rate. In general terms, the more payroll associated with your governing class (the class code with the preponderance of your payroll) the higher your primary threshold will be. The primary threshold is unique to every business. The 2019 EMR formula is heavily weighted by the company's actual primary losses, the claim cost (both paid and reserved) that goes into the calculation up the primary threshold amount. Controlling claim cost and knowing your company's primary threshold is the first step to understanding the EMR.

Expected Loss Rates

The expected loss rate is the factor used to anticipate a class code's claim cost per $100 for the experience rating period. The expected loss rate (ELR) is not to be confused with the pure premium rate (PPR). The ELR differs from the PPR in that the ELR simply measures the basic claim cost for a class code without including loss adjustment expense, excess loss load (capped at $175,000 for X-MOD purposes), and loss development. The PPR includes all of the mentioned above factors and is the rate for which a carrier can expect to pay all of the cost associated with claims in a specific industry. The PPR does not account for the carrier’s overhead, profit, tax, and commissions.

The ELR changes, annually. It’s important to monitor the change; if your expected loss rates go down (from our analysis this is the direction most are going) and if nothing else changes, your EMR will go up. Why is this? Again, without going too deep, in simple terms, your EMR is a ratio of actual losses to expected losses. If your expected losses go down, but your actual losses remain the same, then your EMR will go up.

To illustrate this, consider the following. Actual losses are $25,000 and your expected losses are $25,000 your EMR would be 100. Now, if your actual losses stay the same at $25,000, but your expected losses drop to $20,000, your EMR would now be 125%. (There are other factors that would go into the actual calculation, so your actual EMR would be different – this was just to illustrate the expected losses impact to the EMR.)

In Part 2 of this article, will cover the actual changes to the EMR calculation.

For more information about the EMR, contact Rancho Mesa Insurance Services at (619) 937-0164.